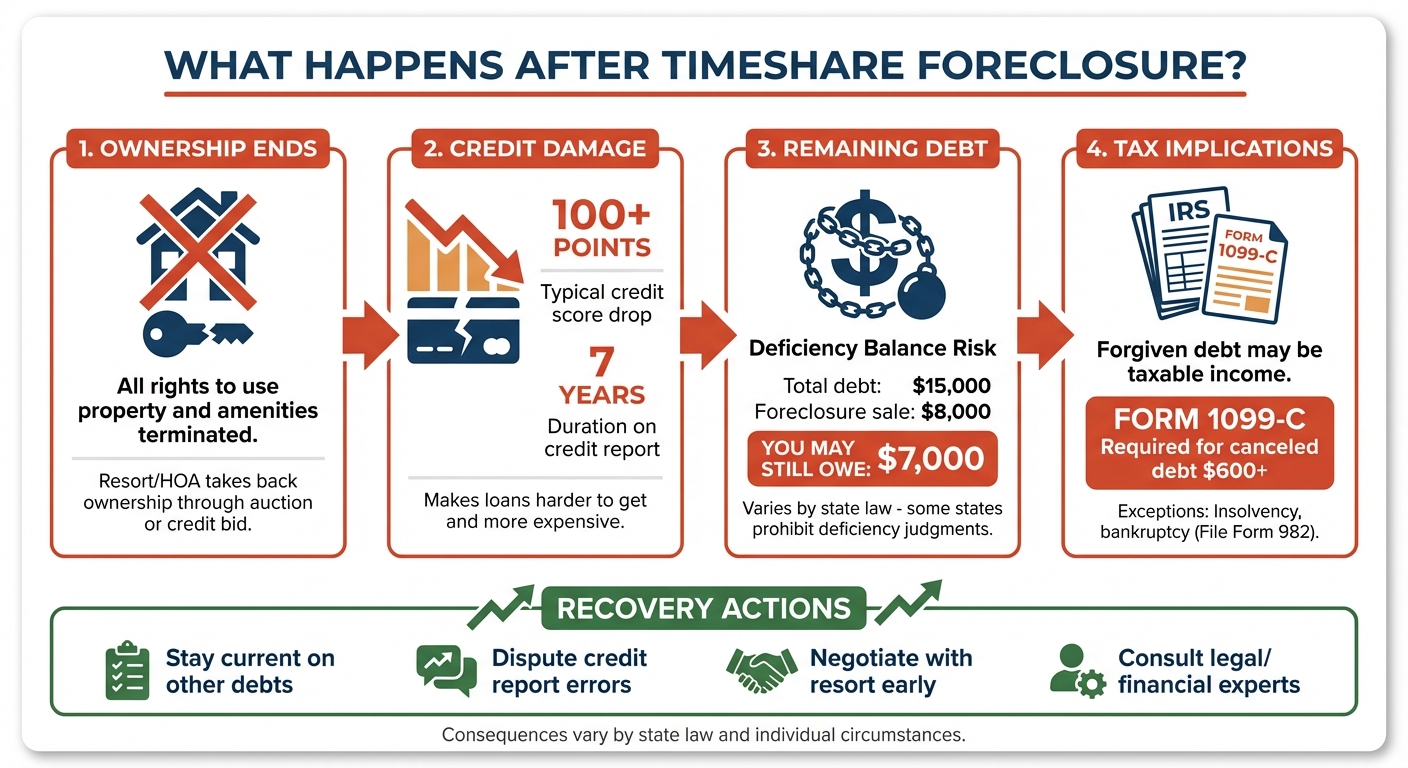

Losing a timeshare through foreclosure can have lasting effects on your finances and credit. Here’s what you need to know:

- Ownership Ends: You lose all rights to use the property or its amenities. The resort or HOA takes back your share, often selling it at auction or keeping it.

- Credit Damage: Foreclosure drops your credit score by 100+ points and stays on your record for 7 years. This can make loans or mortgages harder to get and more expensive.

- Remaining Debt: If the foreclosure sale doesn’t cover your debt, you may owe the difference (a "deficiency balance"). Some states allow lenders to pursue this through legal judgments.

- Tax Implications: Forgiven debt may be taxable as income, requiring you to report it to the IRS. Certain exceptions, like insolvency or bankruptcy, might reduce your tax burden.

To minimize long-term problems, stay current on other debts, dispute credit report errors, and consider negotiating with the resort to avoid foreclosure. Consulting a legal or financial expert can help manage these challenges effectively.

Financial Impact of Timeshare Foreclosure: Credit, Debt, and Tax Consequences

Loss of Ownership and Use Rights

End of Ownership and Usage Rights

When foreclosure is complete, your legal rights to the timeshare officially end. This means you no longer have the ability to book vacations, use the resort’s amenities, or claim ownership. At this point, the resort developer or the homeowners’ association (HOA) takes back your ownership interest. They might sell it at a public auction or keep it through a credit bid.

The process varies depending on the type of timeshare you own. For deeded timeshares, which are considered real property, the foreclosure process follows formal judicial or nonjudicial procedures as outlined by state law. This process ultimately transfers the deed back to the resort.

"With a deeded timeshare, you buy a fraction of the timeshare. You’ll receive a legal deed because your interest is considered real property." – Amy Loftsgordon, Attorney

For right-to-use (RTU) and points-based contracts, which function more like leases, the result is a repossession. Regardless of the type of ownership, defaulting means losing your usage rights. While you won’t be responsible for future fees after foreclosure, any past-due balances can still be enforced.

It’s important to note that these changes apply only to your specific ownership interest. They don’t affect co-owners or the overall operations of the resort.

Effect on Co-Owners and the Resort

Foreclosure impacts only your individual ownership interest. If other family members or co-owners hold separate interests in the same resort or timeshare association, their rights remain unaffected. The resort’s operations also continue as usual, with no disruptions caused by your default. The lien and foreclosure are tied solely to your fractional share and don’t extend to the entire property or to other owners’ stakes. Understanding the implications of losing ownership is key to navigating the financial and credit consequences that follow.

Impact on Credit and Financial Standing

When a timeshare foreclosure happens, it doesn’t just end your ownership rights – it can also lead to long-term financial challenges. Beyond losing access to the property, the effects on your financial record can be significant.

Credit Score Damage

The financial fallout from a timeshare foreclosure is serious. One major consequence is the impact on your credit score. A foreclosure typically causes your FICO score to drop by at least 100 points, and the decline can be even steeper for those with higher starting scores.

"Typically, a foreclosure will drop your FICO credit scores at least 100 points, probably more." – Amy Loftsgordon, Attorney, Nolo

Even if your timeshare developer doesn’t report missed payments directly to credit bureaus, the foreclosure itself will still appear on your record. Foreclosures – whether judicial or nonjudicial – are public records, and credit reporting agencies like Experian, Equifax, and TransUnion regularly update their files with this information. Additionally, any late payments leading up to the foreclosure will also show up on your credit report.

This negative mark stays on your credit report for seven years from the foreclosure’s completion date. While the impact lessens over time, it can still significantly influence your financial options during those years.

Practical Consequences of Credit Damage

The damage to your credit score doesn’t just exist on paper – it has real-world consequences. For example, you might have to wait up to seven years before qualifying for a new residential mortgage. Lenders see foreclosures as a red flag, and many will hesitate to approve loans until a significant amount of time has passed.

Borrowing for other needs also becomes more expensive. Higher interest rates on auto loans and credit cards can add thousands of dollars to your costs over time. On top of that, existing creditors may lower your credit limits or even close accounts after spotting the foreclosure on your record.

"If you’re applying for a job in the financial services or banking industry, a bad credit report might affect your ability to get the job." – Amy Loftsgordon, Attorney, Nolo

The consequences can extend beyond borrowing. In industries like finance and banking, employers often check credit reports as part of the hiring process. A foreclosure on your record could make it harder to land certain jobs.

To help your credit recover, focus on staying current with all your other debts. Consistently paying your bills on time shows lenders that you’ve taken steps to improve your financial habits and can speed up your recovery process.

Remaining Debt and Legal Consequences

Unresolved timeshare debts can lead to more than just credit score damage – they can open the door to legal and collection actions that many owners don’t anticipate. A common misconception is that foreclosure wipes out all financial responsibilities. Unfortunately, foreclosure doesn’t necessarily mean you’re off the hook. Depending on your state’s laws and the type of foreclosure, you might still owe money and face aggressive collection efforts.

Deficiency Balances and Judgments

A deficiency balance occurs when the amount owed on your timeshare (including the mortgage, interest, and fees) exceeds the sales price at foreclosure. For example, if your total debt was $15,000 but the timeshare sold for only $8,000, you’d be left with a $7,000 deficiency.

"The difference between the sale price and the total debt is called a ‘deficiency.’" – Amy Loftsgordon, Attorney, Nolo

In many states, lenders can pursue a deficiency judgment, which is a court order requiring you to pay the leftover balance. Once creditors have this judgment, they can use tools like wage garnishment, bank account levies, or property liens to collect what you owe.

However, laws vary widely by state. For example, in California, anti-deficiency laws (CCP § 580b) protect borrowers from deficiency judgments after timeshare foreclosures. Similarly, in Florida, borrowers are usually not subject to deficiency judgments after a nonjudicial foreclosure, provided they don’t contest the process. The type of foreclosure also plays a role – judicial foreclosures (handled in court) are more likely to result in deficiency judgments than nonjudicial ones (managed outside of court by a trustee).

If the lender chooses not to pursue a judgment, they might write off the remaining debt. But this doesn’t mean you’re in the clear. The IRS could treat the forgiven amount as taxable income, requiring you to report it on your taxes via a 1099-C form. This could lead to a hefty tax bill, so consulting a tax professional is a smart move.

Collections and Legal Actions

Even before foreclosure happens, unpaid maintenance fees and special assessments can trigger collection efforts. Resorts typically start by sending notices, but if payments remain overdue, they often hand the account over to third-party collection agencies. These agencies can be aggressive and may report delinquencies to credit bureaus, which further harms your credit.

Beyond mortgage-related issues, timeshare associations can also sue for unpaid maintenance fees or special assessments. These lawsuits are independent of foreclosure and can result in additional money judgments against you. Once a judgment is issued, the association may take steps like garnishing your wages or levying your bank account to recover the debt.

"Once a court issues a money judgment in favor of the HOA, the HOA might be able to take money out of your bank account or garnish your wages to collect the amount you owe." – Amy Loftsgordon, Attorney, Lawyers.com

To avoid these escalating issues, it’s best to negotiate early. Many resorts are open to alternatives like a "deed in lieu of foreclosure" (also known as a deedback) or a settlement agreement. If you pursue this route, ensure the agreement includes a written waiver or release of liability for any deficiency balance – otherwise, you could still be responsible for the remaining debt. Early action can save you from a cascade of financial and legal troubles.

sbb-itb-d69ac80

Tax Implications and Public Records

Tax Consequences of Forgiven Debt

Facing foreclosure can be tough enough, but it often comes with an extra financial twist: tax liabilities. When a lender forgives a deficiency balance after foreclosure, the IRS considers the forgiven amount as taxable income. If the canceled debt is $600 or more, the lender is required to report it to the IRS using Form 1099-C, and you’ll receive a copy as well.

"Generally, if you owe a debt to someone else and they cancel or forgive that debt for less than its full amount, you are treated for income tax purposes as having income and may have to pay tax on this income." – IRS Publication 4681

How the IRS handles this depends on whether your timeshare loan is classified as recourse or nonrecourse debt. With a recourse loan – where you’re personally liable – the IRS treats the difference between the property’s fair market value and the remaining loan balance as taxable income. For nonrecourse loans, the foreclosure is treated like a sale. If the forgiven debt is greater than the adjusted basis of the property, it could result in a taxable gain.

Thankfully, there are exceptions that could ease the tax burden. If your total liabilities exceeded your assets at the time the debt was forgiven, you might qualify to exclude some or all of the forgiven amount from taxable income. This is known as the insolvency exception. Similarly, debts discharged through a Title 11 bankruptcy case may also be excluded. To claim these exclusions, file Form 982 with your tax return. The IRS Insolvency Worksheet in Publication 4681 can help you determine if you qualify.

Lastly, double-check your Form 1099-C for accuracy. Pay close attention to the canceled debt amount and event codes. If you spot any errors, reach out to your lender immediately to get them corrected.

Legal Recovery and Post-Foreclosure Strategies

Steps to Rebuild Credit and Dispute Errors

Recovering from foreclosure starts with addressing its impact on your credit. A foreclosure on your credit report can drop your FICO score by over 100 points, but rebuilding your credit is possible – starting with payment history.

Begin by regularly reviewing your credit reports to ensure the foreclosure is reported correctly. Credit bureaus update foreclosure information from public records, so if you find errors or outdated details, dispute them directly with the bureaus. As attorney Amy Loftsgordon explains, "You can’t legally remove accurate information from your credit report until it becomes outdated." Be cautious of credit repair scams that claim they can erase accurate foreclosure records for a fee – they can’t do anything you can’t handle yourself.

To rebuild, focus on paying all your bills on time. Using a secured credit card backed by a cash deposit can help establish a positive payment history. Also, keep your credit utilization low – ideally under 30% of your credit limit. Many individuals with excellent credit aim for 10% or less.

Negotiating Settlements and Resolving Debt

Rebuilding credit is just one piece of the puzzle. Tackling outstanding debt is equally important to prevent further legal complications. Reach out to your resort or lender to discuss repayment plans or negotiate for a reduced balance. Another option is a deedback arrangement, where you voluntarily return the property title to the resort. While resorts may resist deedbacks without professional help, legal representation can often make this route more appealing by showing that it’s less costly than a drawn-out foreclosure.

Keep in mind that if a lender forgives your remaining balance, they may issue a 1099-C form, which could count as taxable income. It’s also essential to understand your state’s foreclosure laws. For instance, some states, like Florida, generally bar deficiency judgments in nonjudicial timeshare foreclosures, provided the owner doesn’t contest the process.

How Aaronson Law Firm Can Help

Navigating post-foreclosure challenges can be overwhelming, but specialized legal support can make a significant difference. Aaronson Law Firm offers services to help former timeshare owners recover financially and legally after foreclosure. Their attorneys review credit reports for foreclosure-related inaccuracies and assist clients in disputing errors that unfairly harm credit scores. They also negotiate with resorts to settle outstanding balances, deficiency judgments, or overdue assessments, often through settlement agreements or deedback options.

In cases where resorts pursue deficiency judgments, the firm provides litigation support, including legal demand letters and court representation, to protect clients’ rights. As they emphasize, "Unlike timeshare exit companies, we are actual attorneys. That means that we have a fiduciary and legal obligation to put our client’s interests first." The firm also advises on tax considerations, such as dealing with 1099-C forms issued for forgiven debt. With a free initial consultation, Aaronson Law Firm helps clients explore their options and develop tailored strategies for financial recovery.

Conclusion

Timeshare foreclosure comes with serious financial and legal challenges, including the potential for major credit damage that could affect your ability to secure loans or even find employment. In some states, you might still owe money after the foreclosure sale through deficiency judgments, and any forgiven debt could be treated as taxable income, reported to the IRS on Form 1099-C.

Understanding these consequences is crucial to navigating your recovery. Since foreclosure laws differ widely from state to state, being familiar with the specific regulations where you live can help you prepare for the road ahead. This knowledge allows you to make informed decisions and plan more effectively.

To lessen the financial strain, focus on staying current with debts, disputing any credit report errors, and negotiating settlements when possible. That said, tackling these issues on your own can feel overwhelming, especially when dealing with complicated state laws and potential tax obligations.

Seeking expert legal advice can make a world of difference. An attorney can help protect you from deficiency judgments, negotiate on your behalf, and shield you from scams that often target vulnerable timeshare owners. As attorney Amy Loftsgordon explains, "A lawyer can advise you about ways to potentially keep or dispose of the timeshare or ways to improve your credit after a foreclosure."

Taking action now – whether by consulting professionals, reviewing your credit, or exploring settlement options – can help you regain control of your financial future.

FAQs

What steps can I take to rebuild my credit after a timeshare foreclosure?

Rebuilding your credit after a timeshare foreclosure isn’t an overnight process – it requires patience and steady effort. Start by focusing on the basics: pay your bills on time and stick to a budget that works for your financial situation. These habits lay the foundation for improving your credit over time.

You might also want to look into secured credit cards or low-limit credit lines. These tools can help you rebuild your credit history, as long as you keep your balances low and make payments regularly.

It’s also a good idea to keep an eye on your credit reports. Check them regularly for errors or inaccuracies, and if you spot something wrong, dispute it. Ensuring your credit report is accurate is a key step in improving your credit score.

If the aftermath of the foreclosure feels overwhelming, reaching out to professionals, like Aaronson Law Firm, can provide guidance. They can help you navigate any lingering financial or legal challenges and prevent further damage to your credit.

By staying consistent and following a structured plan, you’ll be on your way to financial recovery and a healthier credit score.

What legal options can help you avoid a deficiency judgment after a timeshare foreclosure?

If you’re worried about a deficiency judgment tied to your timeshare, there are steps you can take to potentially sidestep this situation before foreclosure becomes a reality. For instance, you could rescind the contract during the cancellation period, negotiate a settlement with the timeshare developer, or explore a developer relinquishment program that allows you to voluntarily return the property.

Getting help from a legal professional experienced in timeshare issues can make a big difference. They can guide you through these options, ensuring everything is done properly while helping you avoid financial pitfalls and potential damage to your credit. Legal experts familiar with timeshare laws can offer the support you need to navigate this challenging process.

What are the tax consequences if my timeshare debt is forgiven?

If your timeshare debt is forgiven, the amount canceled is usually treated as taxable income and must be reported to the IRS. In most cases, you’ll receive a Form 1099-C from the lender, which outlines the amount of debt that was forgiven. That said, there are some situations where exceptions or exclusions might apply, such as if you’ve declared bankruptcy or meet the criteria for insolvency.

To fully understand how forgiven timeshare debt could affect your taxes and determine if you qualify for any exclusions, it’s a good idea to consult with a tax professional. They can help you navigate the process and ensure everything is handled correctly.

Related Blog Posts

- How Timeshare Payment Plans Affect Credit Scores

- Timeshare Debt After Cancellation: What To Know

- Timeshare Exit vs. Foreclosure: Credit Impact

- Co-Signer Liability in Timeshare Defaults