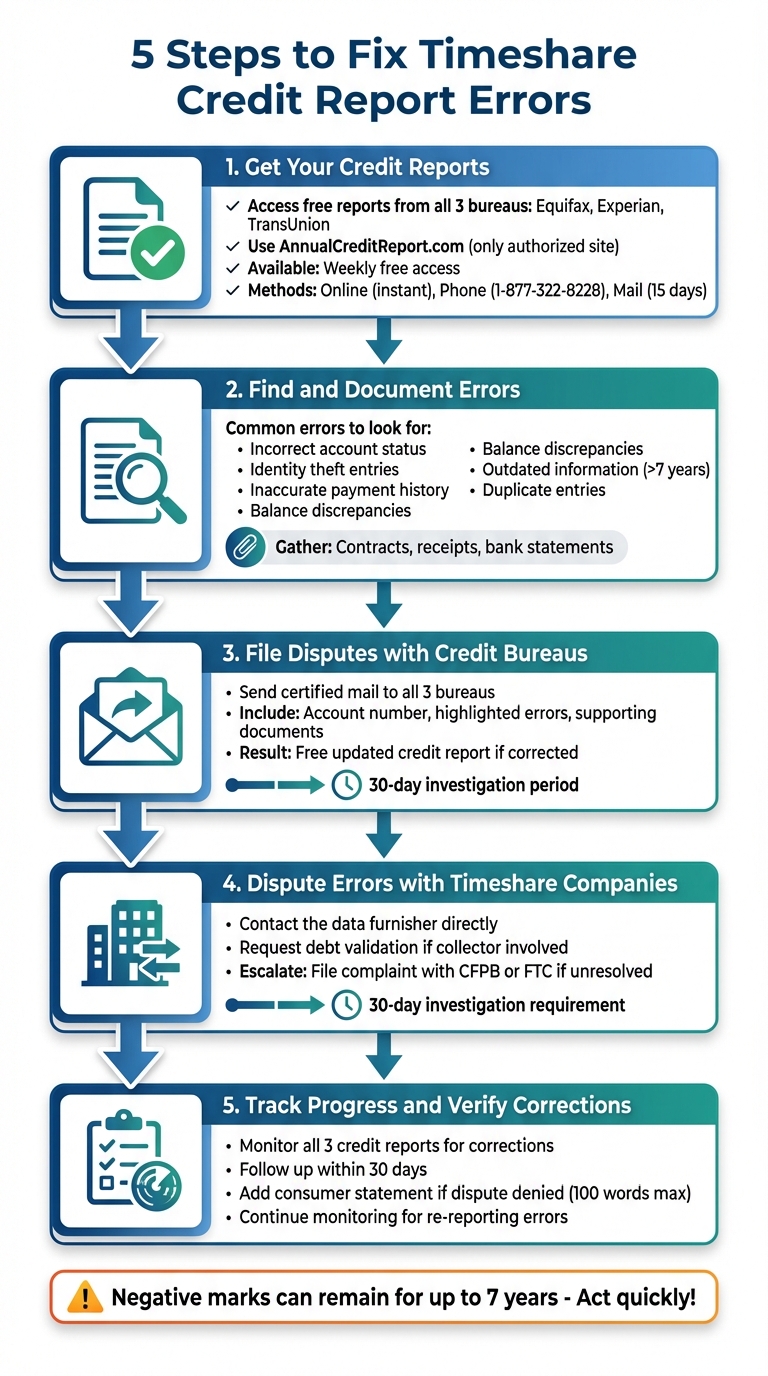

If your credit report contains errors related to a timeshare, it can seriously impact your financial health. These errors often include incorrect balances, duplicate entries, or outdated delinquencies that can harm your credit score for up to seven years. Fixing these issues is essential to protect your ability to secure loans, rentals, or even jobs. Here’s a quick summary of the steps to resolve these errors:

- Get Your Credit Reports: Access free reports from Equifax, Experian, and TransUnion via AnnualCreditReport.com to identify discrepancies.

- Find and Document Errors: Highlight mistakes like duplicate listings, incorrect balances, or outdated negative marks, and gather supporting evidence such as payment receipts.

- File Disputes with Credit Bureaus: Submit dispute letters with proof to each bureau reporting the error, ensuring corrections are made within the 30-day investigation period.

- Dispute Errors with Timeshare Companies: Contact the timeshare company or debt collector directly to resolve issues at the source, and request debt validation if needed.

- Track Progress and Verify Corrections: Follow up on disputes, confirm corrections across all three reports, and monitor for recurring mistakes.

Act quickly to resolve these errors and consider seeking legal help if the issues persist. Fixing timeshare-related credit errors ensures your credit score reflects accurate information, safeguarding your financial future.

5 Steps to Fix Timeshare Credit Report Errors

Step 1: Get Your Credit Reports

Having accurate credit reports is crucial when it comes to spotting and disputing mistakes tied to timeshare contracts. The first step? Take a close look at what’s on your credit reports. Thanks to federal law, you’re entitled to free credit reports from all three major credit bureaus – Equifax, Experian, and TransUnion – once every 12 months. Even better, a permanent program now allows weekly free access to these reports through AnnualCreditReport.com. Plus, through 2026, U.S. consumers can grab six additional free Equifax reports annually.

Why Check All Three Reports?

Each credit bureau gathers information from different sources, which means your timeshare account could show up differently – or not at all – depending on the bureau. The Federal Trade Commission (FTC) explains:

Because each nationwide credit bureau gets its information from different sources, the information in your report from one credit bureau may not be the same as the information in your reports from the other two credit bureaus.

Your timeshare lender or developer might only report to one or two bureaus, leaving the third out entirely. For example, a mistake on your Equifax report might not appear on your Experian or TransUnion ones. If you only check one bureau, you could miss errors elsewhere. Since you’ll need to dispute mistakes separately with each bureau reporting wrong information, reviewing all three reports is the only way to ensure complete accuracy.

How to Access Free Credit Reports

AnnualCreditReport.com is the only website authorized by federal law to provide free credit reports. The FTC clarifies:

AnnualCreditReport.com is the only official site explicitly directed by Federal law to provide them.

There are three ways to request your reports:

- Online for instant access

- By phone at 1-877-322-8228

- By mail by sending a request form to P.O. Box 105281, Atlanta, GA 30348-5281

Phone and mail requests take about 15 days to process. You’ll need to verify your identity by providing your name, address, Social Security number, date of birth, and answering security questions about your financial history.

Stick to AnnualCreditReport.com to avoid scam websites that mimic its name or offer “free” scores or monitoring services. For safety, use a secure connection and a regular computer – not a mobile device – when entering sensitive information like your Social Security number. Once you’ve got your reports, you’ll be ready to identify any timeshare-related errors.

Step 2: Find and Document Errors

Once you have your credit reports in hand, it’s time to carefully review them for any timeshare-related errors. Start by printing out the reports and marking any discrepancies you find – these highlighted areas will be your evidence during the dispute process. Compare each report against your personal records, such as payment receipts, bank statements, and timeshare contracts. This step is crucial for building a solid foundation for your dispute.

Common Timeshare Credit Report Errors

Several types of errors tend to show up in credit reports related to timeshares.

- Incorrect account status: Your timeshare account might be listed as delinquent, in default, or even sent to collections, even if you’ve made payments on time or legally canceled the contract.

- Identity theft entries: Be on the lookout for any timeshare accounts or loans you didn’t open, as these could indicate fraudulent use of your personal information.

- Inaccurate payment history: Check that all payment dates and amounts match your records. Even a single 30-day late payment error can harm your credit score, so it’s important to catch and correct these mistakes.

- Balance discrepancies: The balance reported should accurately reflect your payments and should not include unauthorized fees or maintenance charges that weren’t part of your original agreement.

- Outdated information: Negative marks older than seven years (or 10 years for bankruptcies) should no longer appear on your credit report and need to be removed.

- Duplicate entries: Sometimes, the same timeshare debt is listed twice – once by the developer and again by a collection agency. This duplication unfairly impacts your credit score.

- Incorrect personal details: Errors like misspelled names, wrong addresses, or incorrect Social Security numbers can lead to mixed files, where someone else’s information gets merged with yours.

Gather Supporting Documents

To strengthen your dispute, you’ll need to compile a thorough evidence package. This includes:

- Your original timeshare contract and any related purchase documents, such as closing paperwork and sales materials.

- Receipts for maintenance fees and mortgage payments, along with bank statements showing when payments were made.

- Any correspondence from a cancellation attorney if you’ve worked with one to rescind the contract.

Double-check that the account number on your credit report matches the one on your timeshare member statements. Mismatched numbers can indicate reporting errors. Organize all your documentation in chronological order to make it easier to present your case.

When submitting your dispute, only send copies of your documents – never the originals. Use certified mail with a "return receipt" to ensure you have proof that your materials were received. If a collection agency is involved, you can also request formal debt validation to confirm their legal authority to report the debt. This meticulous preparation will help you build a strong case when contesting errors with credit bureaus or timeshare companies.

Step 3: File Disputes with Credit Bureaus

Once you’ve documented the errors on your credit report, it’s time to dispute them with the three major credit bureaus: Equifax, Experian, and TransUnion. You can file disputes online, by mail, or over the phone – all at no cost, thanks to federal law. While online disputes are quicker and allow you to track updates in real time, mail is often better for complex issues, like timeshare disputes, because it creates a physical record. This can be a lifesaver if legal documentation becomes necessary. The next step? Crafting a clear, effective dispute letter.

How to Write a Dispute Letter

Start your dispute letter by including your full name, current address, and phone number. Be sure to mention the account number of the timeshare or collection account you’re disputing, along with your credit report confirmation number if available. Address each mistake individually. For instance, if your timeshare account shows as overdue but you’ve made all payments on time, clearly state this and explain why the information is wrong.

Attach a copy of your credit report with the errors highlighted, along with any supporting documents such as payment receipts, bank statements, or letters from the timeshare company. Always send copies, not originals, since they won’t be returned. Be specific about what you’re asking for – whether it’s removing inaccurate information or correcting the error. Send your dispute via certified mail with a return receipt requested to ensure you have proof of delivery. Use the following addresses for each bureau:

- Equifax: P.O. Box 740256, Atlanta, GA 30374-0256

- Experian: P.O. Box 4500, Allen, TX 75013

- TransUnion: P.O. Box 2000, Chester, PA 19016

Investigation Timeline

Credit bureaus are required to investigate and respond to your dispute within 30 days. During this time, they send your evidence to the company or lender that originally reported the information – referred to as the "data furnisher." This company will review the evidence, conduct its own investigation, and report back to the bureau. If you submit additional evidence after the process begins, the investigation period may extend to 45 days.

Once the investigation wraps up, the credit bureau must notify you of the results in writing. If the dispute results in a correction, you’ll receive a free updated credit report, which won’t count against your annual free report limit. Additionally, you can ask the bureau to notify anyone who accessed your report in the last six months – or the past two years if it was used for employment purposes – about the correction. Keep all correspondence and documentation on file in case you need it for future reference.

Step 4: Dispute Errors with Timeshare Companies

Disputing errors with credit bureaus is just one part of the process. You also need to address the issue at its source – the timeshare company or debt collector reporting the incorrect information. These entities, known as "furnishers" under federal law, are required to investigate disputes within 30 days of receiving them. Resolving the issue directly with the furnisher can prevent the error from resurfacing, even after the credit bureaus make corrections.

Contact the Company or Collector

Start by gathering all relevant documents, such as your account number, sales agreements, payment receipts, and bank statements. Write a detailed dispute letter including your full name, address, phone number, account number, and a clear explanation of the errors, supported by evidence of timely payments.

Attach copies of your supporting documents (never send originals) and send the dispute via certified mail with a return receipt. The furnisher’s address can typically be found on your credit report. If they confirm the information is inaccurate, they are legally obligated to inform all three credit bureaus to update your file. Keep copies of everything in case you need to escalate the matter later.

If a debt collector is involved, you’ll need to take an additional step to validate the debt.

Request Debt Validation

When a debt collector is reporting the timeshare debt, you’re protected under the Fair Debt Collection Practices Act (FDCPA). Send them a debt validation letter requesting proof that the debt is legitimate. This includes documentation from the original creditor, the amount owed, and verification that they have the right to collect the debt. Until they provide this information, they must pause all collection activities.

If these steps don’t resolve the issue, you might want to consult Aaronson Law Firm for help with legal demand letters and credit protection.

Should the company fail to correct the error or ignore your dispute, you can escalate the matter by filing a complaint with the CFPB (Consumer Financial Protection Bureau) or FTC (Federal Trade Commission). Additionally, if the company continues reporting the account, they are required to mark it as "disputed" on your credit report. However, timeshare developers can be unresponsive to individual disputes, which is why professional legal assistance can make a difference.

Once you’ve addressed this step, move on to Step 5 to track your progress and ensure corrections have been made.

sbb-itb-d69ac80

Step 5: Track Progress and Verify Corrections

Once you’ve filed your disputes, it’s important to stay on top of the process and confirm that corrections are made on all three of your credit reports. Timeshare errors can have lasting effects, so taking these steps ensures they don’t continue to harm your credit. Credit bureaus typically have up to 30 days to investigate disputes, but that doesn’t mean you should sit back and wait.

Follow Up on Your Disputes

After submitting your disputes, keep your confirmation numbers handy and log into your accounts regularly to check for updates. If you filed your disputes online with Equifax, TransUnion, or Experian, you might also receive email notifications about the status of your cases.

Once the investigation wraps up, the credit bureau will send you written results. Carefully review your updated credit report to confirm that the necessary corrections have been made. If the timeshare company admitted their error, they are legally obligated to inform all three credit bureaus. Make sure the corrections appear consistently across all three reports.

Even after corrections are made, continue monitoring your credit reports in the months ahead. Timeshare companies sometimes mistakenly re-report incorrect information during future billing cycles. Keeping an eye on your reports ensures the problem doesn’t resurface and helps you address any lingering issues promptly.

Add a Statement if Disputes Are Denied

If the credit bureau denies your dispute, you still have options. One of them is to add a consumer statement to your credit file. This brief statement – usually capped at 100 words – allows you to explain your perspective. While it won’t affect your credit score, it provides future lenders with additional context when they review your report.

If your dispute is rejected, the credit bureau must notify you within five business days. If errors remain uncorrected despite clear evidence, escalate the situation by filing a formal complaint with the Consumer Financial Protection Bureau (CFPB). If you’re dealing with a timeshare company that refuses to fix its records, reaching out to Aaronson Law Firm can provide you with expert legal assistance to resolve the issue.

How Aaronson Law Firm Can Help

If the steps you’ve tried on your own aren’t enough, bringing in professional legal help can make all the difference. Aaronson Law Firm focuses on timeshare contract cancellations and provides legal letters designed to protect your credit while resolving disputes. By building on the steps you’ve already taken, the firm offers personalized legal strategies to address your timeshare credit issues and prevent future reporting mistakes.

Legal Demand Letters and Credit Protection

Aaronson Law Firm creates formal legal position letters that clearly outline your legal claims and defenses against timeshare developers. These aren’t cookie-cutter documents – they’re custom-crafted by licensed attorneys. What sets them apart is the authority behind them, as these attorneys have the legal power to sue or countersue if needed.

"Emphatically, without the ability to sue or countersue the timeshare developer through a timeshare lawyer you have NO legal protection or leverage." – Aaronson Law Firm

These legal letters are sent under the Fair Credit Reporting Act to help reduce the risk of damage to your credit report during the dispute. While no one can promise complete credit protection, these letters significantly strengthen your position when dealing with credit bureaus and timeshare companies.

Aaronson Law Firm also provides a free eBook titled "The Credit Dispute Process", which walks you through steps to review your credit report and address any misleading information tied to timeshare mortgages. Along with these resources, you have access to expert advice at no cost.

Free Consultations for Timeshare Problems

Aaronson Law Firm offers free consultations where an attorney reviews your specific timeshare situation and helps you understand your legal options. During this consultation, you’ll receive a clear plan of action tailored to your case.

To make the most of your consultation, gather all relevant documents ahead of time. This includes account numbers, sales details, names of representatives, and any paperwork you received during the purchase. Visit Aaronson Law Firm to schedule your free consultation today.

Conclusion

Taking a methodical approach is key to addressing timeshare credit errors. By following the outlined steps, you can work toward removing harmful inaccuracies from your credit report. Keep in mind, negative marks can remain on your report for up to seven years, so acting quickly is essential.

Beyond fixing errors, protecting your credit score should be a top priority. Your credit score impacts many aspects of life – loan interest rates, rental applications, and even job opportunities. Incorrect timeshare data can lead to unnecessary fees and distorted reports that slow down your financial progress. Taking action now can help you break free from these challenges and rebuild your credit profile.

"Whether you are grappling with mounting fees, inaccurate reporting, or simply wish to clear up your credit profile, this resource offers precise, actionable guidance to help you regain control of your financial future." – Aaronson Law Firm

If these steps don’t resolve the problem, seeking professional legal help might be your best option. Licensed attorneys can take legal action against timeshare developers, giving you the upper hand. Aaronson Law Firm provides free consultations to assess your situation and create a tailored plan to address your concerns. Visit Aaronson Law Firm to schedule your consultation and take a proactive step toward protecting your financial future.

FAQs

Will a timeshare credit error lower my score?

Yes, a timeshare credit error can hurt your credit score. Problems like foreclosure or incorrect account details being reported can negatively impact your credit profile, dragging down your score. Acting quickly to resolve these issues is crucial to safeguard your financial well-being.

What proof should I include with my dispute?

When challenging credit report inaccuracies tied to timeshare contracts, it’s crucial to provide supporting documents. These may include copies of the timeshare agreement, payment records, any correspondence with the timeshare company, and relevant legal documents. Such evidence can bolster your case and improve your chances of resolving the issue. For tailored guidance on timeshare-related matters, it’s wise to consult a legal professional with expertise in this field.

What if the bureau keeps the error on my report?

If a credit bureau won’t remove an error from your credit report, it’s time to escalate the matter. Keep submitting written disputes, including all relevant supporting documents, to reinforce your case. If the issue persists, you have other options: you can file a complaint with the Consumer Financial Protection Bureau (CFPB) or consult a legal professional for assistance.

For credit report issues tied to timeshares, Aaronson Law Firm provides legal services aimed at correcting errors and safeguarding your credit.

Related Blog Posts

- Timeshare Exit Checklist: Protecting Your Credit Score

- How Timeshare Payment Plans Affect Credit Scores

- Timeshare Exit vs. Foreclosure: Credit Impact

- Maintaining Positive Credit After Timeshare Cancellation