If you’re dealing with a timeshare issue, knowing whether to contact the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC) is key. Here’s the breakdown:

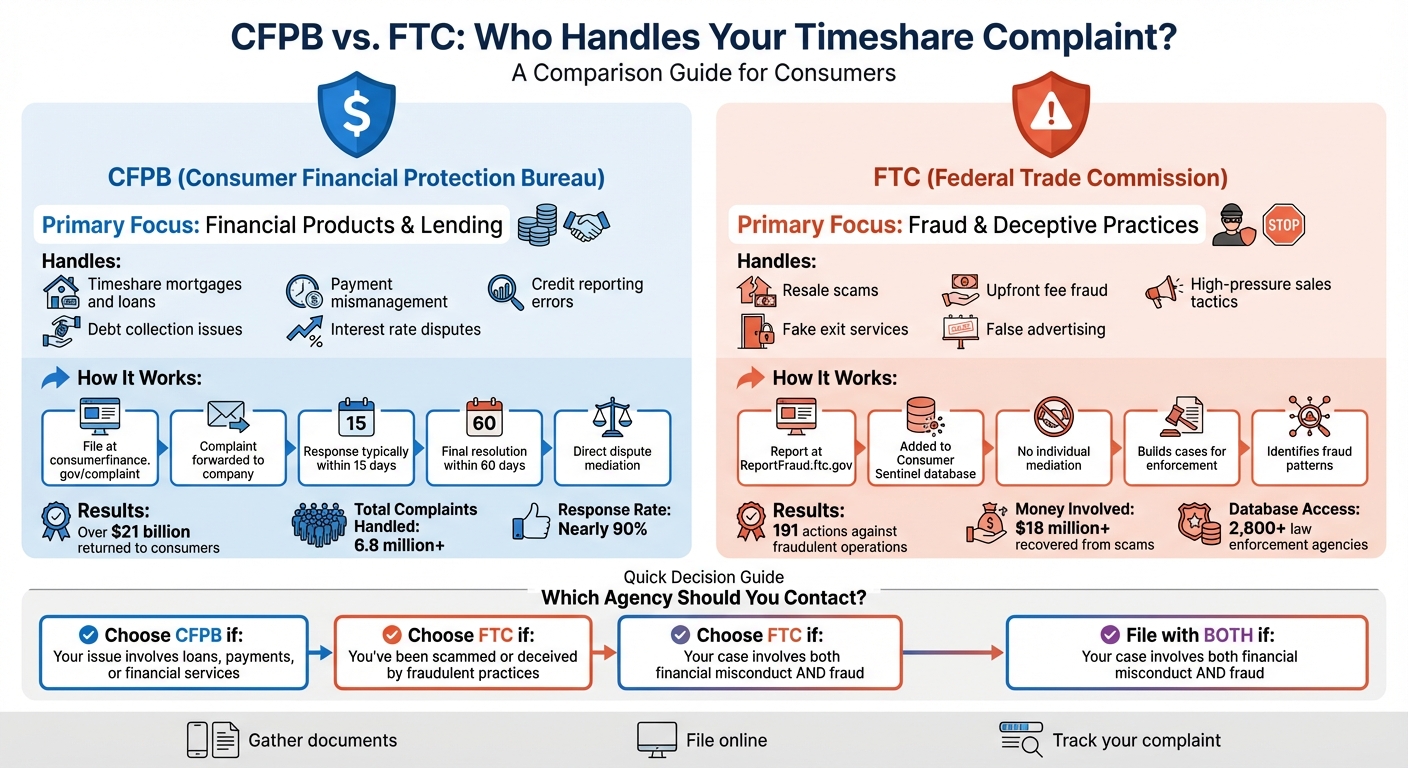

- CFPB: Handles complaints about financial products tied to timeshares, like loans, mortgages, or debt collection. Example: If your timeshare lender mishandles payments or adds unexpected fees.

- FTC: Focuses on fraud and scams, such as false resale promises or upfront fees for exit services. Example: If a company charges you thousands for a "guaranteed" timeshare sale but vanishes.

Quick Overview of Each Agency:

- CFPB: Offers direct dispute resolution with companies. Most complaints receive a response within 15 days.

- FTC: Investigates fraud trends and takes legal action but doesn’t mediate individual disputes.

Key Tip: File with the CFPB for financial disputes and with the FTC for fraud or deceptive practices. Both agencies play distinct roles but work toward protecting consumers from timeshare-related issues.

CFPB vs FTC: Which Agency Handles Your Timeshare Complaint

CFPB’s Role in Timeshare Financing Complaints

Authority Over Financial Misconduct

The Consumer Financial Protection Bureau (CFPB) was established to ensure federal consumer financial laws are enforced effectively. When it comes to timeshares, the CFPB keeps a close watch on the financial products tied to these agreements – things like mortgages, personal loans, or debt collection practices.

The Bureau has the power to address unfair, deceptive, or abusive practices (UDAAP) in the financial sector. This includes tackling issues like high-interest loans tied to timeshares, questionable lending practices, and violations of laws like the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA), which regulate disclosures and mortgage servicing.

What makes the CFPB’s role even more impactful is its oversight of not just traditional banks but also non-bank entities like mortgage servicers and debt collectors involved in timeshare financing. With this broad authority, the CFPB plays a critical role in protecting consumers from financial misconduct in the timeshare industry.

How to File a Timeshare Financing Complaint

Filing a complaint with the CFPB is a simple process. You can submit your complaint online at consumerfinance.gov/complaint, which usually takes about 7–10 minutes, or call 411-2372 for help in over 180 languages. Once filed, the CFPB forwards your complaint to the financial company, requiring them to provide a response.

Before filing, gather all relevant documents, such as account statements, loan agreements, and any communication with the lender. You can upload up to 50 pages of supporting materials. Be as detailed as possible – include dates, dollar amounts, and a clear explanation of the issue. While the CFPB encourages trying to resolve disputes directly with the company first, its complaint system offers a formal way to escalate unresolved issues.

Typically, companies respond within 15 days, and you have 60 days to review their reply. For example, in 2023, David Biddle from Philadelphia resolved a $27,500 fraudulent loan issue through the CFPB. After months of back-and-forth with the lender, he filed a complaint, and the matter was resolved within nine business days, with the account closed.

Since January 2023, consumers have filed roughly 4.8 million complaints with the CFPB, with nearly 90% receiving responses. Additionally, the CFPB’s Consumer Complaint Database, which publishes anonymous complaint details, helps highlight recurring issues and holds companies accountable for their actions.

FTC’s Role in Combating Timeshare Scams and Deceptive Practices

Enforcement Against Scams and Fraud

The FTC plays a crucial role in tackling deceptive sales tactics and outright scams in the timeshare industry. Unlike the CFPB, which focuses on financing issues, the FTC’s authority comes from Section 5(a) of the FTC Act and the Telemarketing Sales Rule, both of which regulate misleading marketing practices.

The agency uses its legal powers to put a stop to fraudulent activities. Under Section 13(b) of the FTC Act, it can seek court orders to halt illegal operations and freeze assets. If the FTC can prove a company’s actions are "dishonest or fraudulent", it may pursue court-ordered refunds for victims under Section 19. Additionally, the FTC can hold internal hearings before an Administrative Law Judge to issue cease-and-desist orders.

In May 2013, the FTC filed a complaint against Resort Solution Trust Inc. in the U.S. District Court for the Middle District of Florida. The company, led by Lincoln Renwick II and Anthony Talavera, allegedly tricked thousands of consumers into paying up-front fees ranging from $800 to $3,400 by falsely promising they had ready buyers. The court intervened, halting these practices, freezing the company’s assets, and placing it into temporary receivership. That same month, the FTC, alongside the Florida Attorney General, sued Vacation Communications Group LLC for charging consumers $1,600 to $2,200 based on similar false claims. The court froze the operation’s U.S. assets.

"Con artists take advantage of timeshare owners who have been in tough financial straits and are desperate to sell their timeshares. They persuade owners to pay fat up-front fees by saying they have someone ready to buy the property, but that’s a lie." – Charles A. Harwood, Acting Director of the FTC’s Bureau of Consumer Protection

The FTC often works with other jurisdictions to strengthen its enforcement. For example, in a multinational effort, the FTC and its partners announced 191 actions aimed at shutting down fraudulent timeshare resale operations and travel scams. These cases included operations accused of taking more than $18 million from consumers across the country.

Reporting Timeshare Fraud to the FTC

The FTC makes it simple to report timeshare fraud. Visit ReportFraud.ftc.gov to file complaints about scams, deceptive practices, or unwanted calls. Unlike the CFPB, the FTC doesn’t mediate individual disputes but uses your report to build cases against fraudulent companies. Your complaint is added to Consumer Sentinel, a secure database used by over 2,800 law enforcement agencies around the world.

These reports are vital – they help the FTC identify patterns of misconduct that could lead to major investigations and legal action. Before filing, gather any relevant documents, such as contracts, emails, or call logs with dates and names. Once your report is submitted, the FTC provides immediate guidance on protecting yourself moving forward.

"Our message to timeshare owners is simple: never pay for a promise, get everything in writing first, and pay only after your unit is sold." – Charles A. Harwood, Acting Director of the FTC’s Bureau of Consumer Protection

Do your homework before paying anything. Look up the company online with terms like "scam" or "complaint", and check with your state attorney general or local consumer protection office. Avoid paying upfront fees – work only with resellers who charge after the timeshare is sold. If an upfront fee is required, make sure the refund policy is clearly outlined in writing. Confirm that the reseller’s agents are licensed real estate brokers in the state where your timeshare is located, and always get every agreement in writing – verbal promises are not enough.

Key Differences Between CFPB and FTC in Handling Timeshare Complaints

Comparison of Authority and Focus Areas

The Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) play distinct roles when it comes to addressing timeshare complaints. The CFPB mainly handles issues tied to financing, such as mortgages, loan servicing, debt collection, and errors in credit reporting. If your timeshare problem involves a bank or lender, the CFPB is the agency to turn to.

The FTC, on the other hand, focuses on fraud and deceptive practices. This includes scams like fake timeshare resale offers, bogus exit services that demand hefty upfront fees, and misleading sales presentations that misrepresent what buyers are signing up for.

| Feature | CFPB | FTC |

|---|---|---|

| Primary Focus | Financial products, lending, and debt issues | Fraud, scams, and deceptive marketing |

| Timeshare Issues | Loan interest rates, mortgage disputes, credit reporting errors | Resale scams, fake exit services, high-pressure sales tactics |

| Resolution Process | Forwards complaints to companies for formal responses (usually within 15 days) | Collects reports to identify fraud patterns for enforcement |

| Typical Outcome | Possible refunds, debt relief, or corrections | Market-wide enforcement or settlements |

Since its inception, the CFPB has returned over $21 billion to consumers, while the FTC has taken action to shut down fraudulent timeshare resale schemes. These differences highlight not just their focus areas but also the ways they interact with consumers.

Filing Processes and Consumer Experience

The differences between the CFPB and FTC extend to how they handle complaints. Filing with the CFPB means your issue is forwarded directly to the financial institution involved. The company is obligated to respond, often within 15 days, and must provide a final resolution within 60 days. Throughout the process, you receive updates and have the opportunity to review and provide feedback on the company’s response.

"Most companies respond within 15 days." – Consumer Financial Protection Bureau

The FTC takes a different approach. When you report fraud through ReportFraud.ftc.gov, your complaint is added to the Consumer Sentinel database, which is accessible to over 2,800 law enforcement agencies. Unlike the CFPB, the FTC does not mediate disputes or contact companies on your behalf. Instead, your report helps the FTC identify fraud trends and take action against fraudulent businesses.

The CFPB has handled over 6.8 million consumer complaints, offering a direct path to resolving financial disputes. Meanwhile, the FTC focuses on large-scale enforcement, aiming to disrupt scams and deceptive practices at their roots.

Example Cases to Illustrate Agency Roles

Real-life cases help illustrate how these agencies operate. For example:

- In November 2022, the FTC took action against Consumer Protection Law for targeting older adults with fraudulent timeshare exit services.

- In December 2021, the CFPB fined LendUp $100,000 and ordered it to stop lending after finding deceptive marketing and fair lending violations.

- In September 2025, the FTC issued alerts about scammers contacting timeshare owners with fake offers of "interested buyers", demanding thousands upfront for nonexistent "taxes" or "closing costs."

These cases highlight the clear division of responsibilities: the CFPB deals with financial disputes, while the FTC tackles scams and deceptive practices.

sbb-itb-d69ac80

When to File a Complaint with CFPB vs. FTC

Assessing the Nature of the Complaint

Deciding whether to file a complaint with the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC) depends on the type of issue you’re facing. The CFPB focuses on financial products, while the FTC tackles deceptive or fraudulent business practices. Here’s how to figure out where to take your complaint:

- If your concern involves a loan, payment processing, or debt collection, it’s likely a financial product issue – this is where the CFPB steps in.

- If you’re dealing with lies, fraud, or aggressive sales tactics designed to take your money, the FTC is the right agency to contact.

For example, if you’re disputing interest rates on a timeshare mortgage, addressing errors on your credit report, or dealing with payment mismanagement by a mortgage servicer, the CFPB is your go-to. On the other hand, if a company promised to sell your timeshare but disappeared after charging an upfront fee, or if you were pressured into signing a contract during a high-pressure sales pitch, the FTC should handle your complaint.

"If another agency would be better able to assist, we’ll send it to them and let you know." – Consumer Financial Protection Bureau

Knowing which agency to approach is crucial. Below are specific examples to help you decide.

Examples of Specific Scenarios

File your complaint with the CFPB if:

- Your lender reports a late payment you actually made on time.

- A debt collector is harassing you with frequent calls or contacting your employer about your timeshare debt.

- Your timeshare mortgage servicer is mismanaging payments, adding unexpected fees, or causing credit report errors tied to your account.

File your complaint with the FTC if:

- A company claimed to have a buyer for your timeshare but demanded upfront fees for "taxes" or "closing costs" and then vanished.

- An exit company charged you thousands of dollars – sometimes up to $80,000 – and stopped responding after payment.

- A salesperson misled you by claiming the timeshare was a "great investment" that would increase in value.

- You were pressured into a contract through "today only" deals or false prize offers during a sales presentation.

Before filing a complaint, reach out to the timeshare developer directly and verify the licensing of any resale agents. It’s also a good idea to search the company name online with terms like "scam" or "complaint" to see if others have experienced similar problems.

How Aaronson Law Firm Can Assist with Regulatory Complaints

Legal Support for Filing Complaints

Aaronson Law Firm offers personalized legal assistance to navigate the complexities of filing regulatory complaints. Whether your issue involves deceptive marketing or financial misconduct, their team ensures you approach the appropriate agency for resolution.

The firm carefully reviews your contract for unfair, deceptive, or abusive acts or practices (UDAAP) under the jurisdiction of the CFPB or instances of fraud and deceptive marketing addressed by the FTC. For example, if you’re dealing with credit reporting errors or issues with a mortgage servicer, they help compile the detailed documentation required by the CFPB. On the other hand, if you’ve fallen victim to a resale scam or an exit company charging upfront fees ranging from $5,000 to $80,000, they assist in reporting the fraud to the FTC through ReportFraud.ftc.gov while building a legal case to recover your losses.

The firm also evaluates your right of rescission or cooling-off period under state law, determining whether your contract can be canceled without needing regulatory intervention. If formal cancellation is required, they ensure your cancellation letter is sent via certified mail with a return receipt, creating the necessary legal record to enforce your rights.

Timeshare Contract Cancellation Services

Aaronson Law Firm also specializes in timeshare contract cancellation, often stemming from regulatory actions. They begin with a free consultation to assess your situation and craft a legal strategy tailored to your needs. This includes drafting legal demand letters – referred to as Rescission Predicate Correspondence – to formally notify the timeshare company of your intent to cancel, leveraging relevant consumer protection laws.

Their credit protection services shield you from the fallout caused by fraudulent exit companies that advise owners to stop paying their mortgage or maintenance fees. Such advice often results in debt collection harassment and damage to your credit. Aaronson Law Firm works to protect your credit while pursuing legitimate cancellation. If litigation becomes necessary, they are prepared to fight for your contract release in court.

Conclusion

Knowing which federal agency to contact for your timeshare complaint can make a big difference in resolving the issue. For financial problems – like predatory lending, mortgage disputes, or credit reporting errors tied to timeshare debt – the CFPB is the right resource. On the other hand, the FTC handles cases involving scams, such as fraudulent services requiring upfront fees.

In many fraud cases, filing complaints with both agencies is a smart approach. These organizations share information with law enforcement, helping to identify and track misconduct across the timeshare industry.

However, filing regulatory complaints alone won’t instantly cancel an unwanted timeshare. While these agencies investigate and take action against bad actors, you may still be bound by your contract. This is where expert legal help becomes crucial. Firms like Aaronson Law Firm focus on timeshare contract cancellation, offering guidance to protect your credit and financial well-being.

Before agreeing to any upfront fees or signing new contracts, always get the terms in writing and check the company’s reputation. You can also contact your resort developer directly to explore official exit programs. If you’ve been scammed or need assistance canceling a contract, Aaronson Law Firm can provide the legal support you need.

FAQs

Who should I contact about my timeshare complaint: the CFPB or the FTC?

Deciding who to contact – CFPB or FTC – depends on the specific issue you’re facing with your timeshare. If your problem involves financing, like hidden fees, billing errors, or unclear loan terms, the CFPB is your go-to agency. However, if you’re dealing with scams, resale fraud, or misleading sales practices, the FTC is better equipped to handle those concerns.

If you’re feeling uncertain about the next steps or need personalized advice, reaching out to a legal professional can provide clarity and guidance tailored to your situation.

Who handles timeshare complaints: the CFPB or the FTC?

The Consumer Financial Protection Bureau (CFPB) deals with complaints tied to timeshare financing, including concerns like billing errors, unexpected fees, and unclear loan terms. Meanwhile, the Federal Trade Commission (FTC) handles problems such as deceptive sales tactics, resale scams, and fraud within the timeshare market.

If you’re dealing with a timeshare problem, knowing the right agency to contact can make the process smoother. For help with canceling a timeshare contract, seeking advice from a law firm that specializes in this area can be a smart move.

What should I do before reporting a timeshare scam?

Before you report a timeshare scam, there are a few critical steps you should take to strengthen your case:

- Look into the company: Investigate its background and reputation. Check for customer complaints, online reviews, or any warning signs such as requests for upfront fees, guarantees of quick sales, or promises of unusually high returns.

- Organize your evidence: Gather all relevant materials, including contracts, email correspondence, payment records, and advertisements. These documents will be crucial in supporting your claim.

- Stop making payments: Hold off on sending any more money or providing personal details until you’ve confirmed the company’s legitimacy.

After completing these steps, report the scam to official organizations like the Federal Trade Commission (FTC). This can help protect others and ensure the issue is addressed appropriately.

Related Blog Posts

- FTC Role in Timeshare Regulation

- How Consumer Protection Laws Impact Timeshare Complaints

- How to File a CFPB Complaint for Timeshare Issues

- FTC vs. State Agencies: Who Regulates What?