If a company asks you to pay before your timeshare is sold, that is the biggest warning sign. In many resale scams, owners lose hundreds or thousands of dollars in upfront fees and still keep the timeshare, the maintenance bills, or both.

Here’s the short version:

- Federal law can apply when resale companies use calls, texts, emails, or online ads to make false promises.

- State law often controls the contract itself, including disclosures, cancellation rights, escrow rules, and licensing.

- You may still be on the hook for fees and contract duties unless the resort or developer gives a formal release.

- Fast action matters if you want a refund, chargeback, rescission, or to file a complaint.

- Your records matter: keep contracts, receipts, emails, texts, screenshots, and call logs.

A few facts stand out:

- Annual maintenance fees can run from a few hundred dollars to several thousand dollars per year.

- Consumer fraud deadlines are often around 2 to 4 years, though timing changes by state and claim type.

- Chargeback windows can be short, so waiting can cost you a refund path.

If I were reviewing a resale offer, I’d focus on five things right away:

- Was I promised a buyer without proof?

- Am I being asked to pay upfront?

- Does the contract clearly explain fees, refunds, and cancellation?

- Is money being held in escrow where state law requires it?

- Did I get a formal release from my original timeshare contract?

Quick Comparison

| Area | What it does | What to watch for |

|---|---|---|

| Federal consumer law | Bars deceptive sales tactics and false claims | Fake buyers, hidden fees, sales pressure |

| Telemarketing rules | Limits abuse in sales calls and some fee practices | Calls demanding payment before any sale |

| State consumer fraud law | Gives owners ways to sue or seek refunds | Misleading ads, false promises, contract tricks |

| State timeshare law | May cover disclosures, cancellation, and escrow | Missing refund terms, weak transfer steps |

| Licensing rules | Controls who may market or sell for others | Unlicensed resellers taking fees |

Bottom line: timeshare resale trouble usually comes down to bad contracts, false promises, or both. If money has already been paid, or if the resale did not end your original duties, I’d stop contact with the seller, gather every record, and look at chargebacks, agency complaints, and legal help right away.

sbb-itb-d69ac80

Federal Rules That Target Timeshare Resale Scams

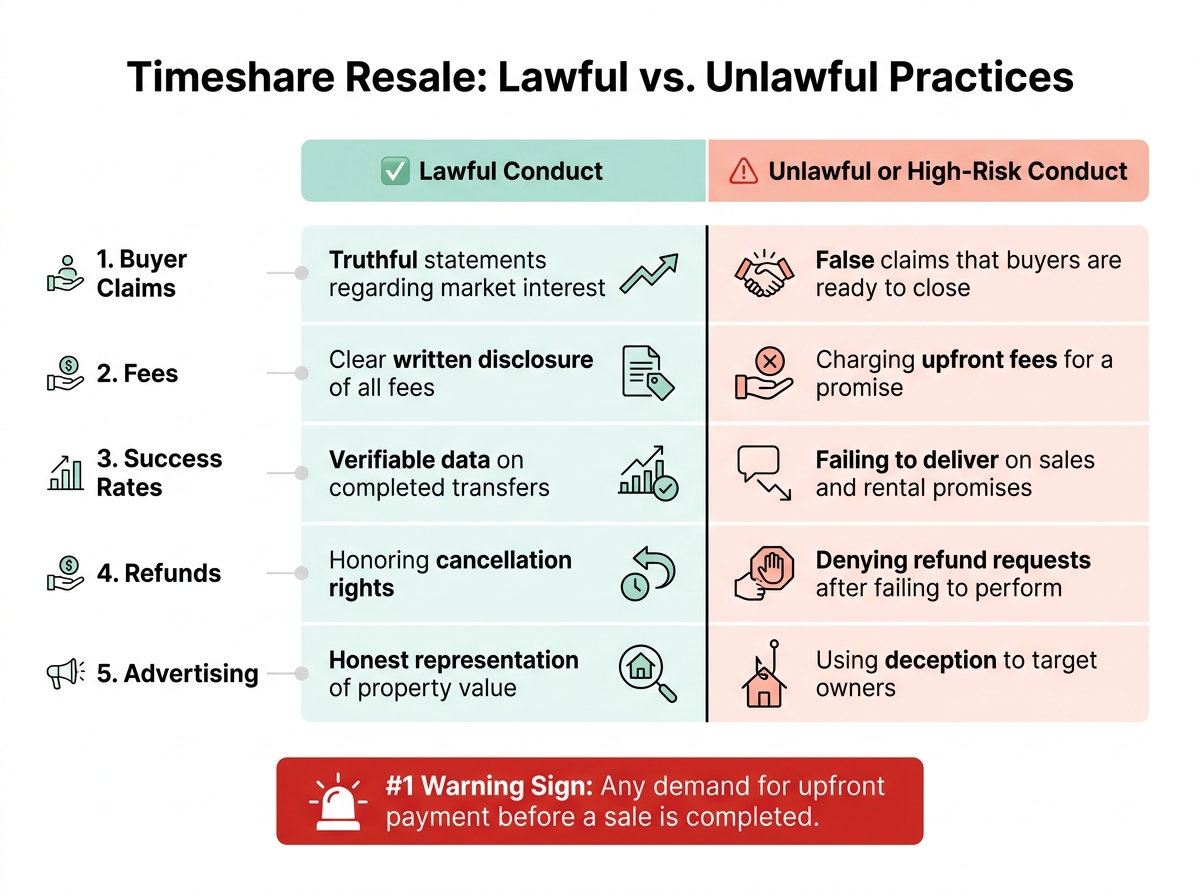

Timeshare Resale Scams: Lawful vs. Unlawful Practices at a Glance

Federal law comes into play when resale companies market across state lines through phone calls, texts, emails, or online ads. For most owners, the biggest danger is simple: an upfront-payment demand. The pitch is usually the same. The company says it already has a buyer or renter lined up and only needs you to pay a fee before the deal can move forward.

That fee might be called a listing fee, marketing fee, or closing fee. But the pattern is what matters. You pay first, and the sale never happens.

FTC Warning Signs in Timeshare Resale Offers

One of the clearest warning signs is an unexpected contact from a company claiming a buyer is ready to close. Then comes the catch: you must send money before anything happens. Deceptive resale companies often ask for upfront fees before any real buyer exists. In many cases, the promised sale or rental never materializes.

Other warning signs show up fast:

- Inflated claims about your timeshare’s value or market demand

- Pressure to pay right away

- Vague answers when you ask for proof

- No written support for the claimed buyer

Before you sign anything or send money, verify the company’s claims and review its complaint history with regulators. Ask for written proof of any buyer claim.

Those tactics often lead straight to telemarketing violations and advance-fee complaints.

Telemarketing and Advance-Fee Practices Under Federal Law

Federal telemarketing rules prohibit deceptive sales calls, false buyer claims, and hidden fees. If a company misrepresents buyer interest, hides fees, or makes false claims about past results, that can trigger federal enforcement. The FTC has repeatedly shut down deceptive timeshare resale operators.

Do not pay upfront for an unverified promise of a sale or rental.

The table below shows the difference between lawful conduct and the kinds of tactics that put owners at risk.

| Practice area | Lawful conduct | Unlawful or high-risk conduct |

|---|---|---|

| Buyer claims | Truthful statements regarding market interest | False claims that buyers are ready to close |

| Fees | Clear written disclosure of all fees | Charging upfront fees for a promise |

| Success rates | Verifiable data on completed transfers | Failing to deliver on sales and rental promises |

| Refunds | Honoring cancellation rights | Denying requests for refunds after failing to perform |

| Advertising | Honest representation of property value | Using deception to target owners |

What Federal Enforcement Can Do for Consumers

FTC and state actions can stop deceptive operators and support refunds. That matters. Still, federal enforcement does not always unwind your contract or repair credit damage. If you’ve already paid and suspect fraud, you may still need to take individual legal action.

Federal action may stop the scam, but state disclosure, escrow, and cancellation rules often decide whether an owner can recover money or unwind the deal.

State Timeshare Resale Laws: Disclosures, Cancellation Rights, and Escrow Protections

Federal law sets the floor. But in most cases, state law is what shapes the deal that lands in front of you.

That includes contract terms, cancellation rights, and escrow rules. And those details can make the difference between getting out of a bad resale deal and getting stuck with one. The catch? Rules change from state to state, so it matters where the deal is governed and which state’s statutes apply.

Required Disclosures in Resale Advertising and Service Contracts

Many states require resale ads and service contracts to spell out material terms in plain view.

That can include:

- Fees

- Refund limits

- Whether any buyer actually exists

This matters because misleading resale ads often bury the ugly parts of the deal. A company may hint that a buyer is lined up, gloss over refund limits, or make fees seem smaller than they are.

And those disclosure rules hit even harder when the contract also cuts down your right to cancel. If the fine print is fuzzy, that’s not a small issue. It’s often the whole game.

Cancellation Periods and Limits on Waiving Consumer Rights

Some states give owners cancellation rights for timeshare-related agreements. But the details turn on the type of contract and the statute that applies.

Put simply, cancellation rights are state-specific. They depend on both the governing law and how the contract is classified. That’s why owners should read the cancellation language with care and avoid signing on the spot.

If a company says there’s no meaningful way to back out, don’t just take its word for it. Check that claim before you pay anything.

Advance Fees, Escrow Accounts, and Transfer Safeguards

One of the biggest red flags is a demand for an advance fee before a sale or rental is finished.

That’s a common play. Bad actors often ask for hundreds or thousands of dollars upfront, then never complete the transfer. Some states push back on that by requiring escrow or other transfer controls before funds can be released. That gives owners one more layer of protection and limits what a resale company can do with the money before the transfer is confirmed.

When a company wants money before a transfer and can’t show proof of progress, the next move is to review the enforcement options available under state and federal law.

Enforcement, Consumer Remedies, and How to Document a Resale Problem

If a resale pitch has crossed the line into deception, the next step is simple: figure out who can act and what you may be able to get back.

Who Enforces Timeshare Resale Laws

More than one agency may step in here, and each one has a different job.

When a resale company ignores disclosure, escrow, or cancellation rules, enforcement and recovery options start to matter fast. The FTC looks at national patterns, especially when conduct crosses state lines. The FTC can stop deceptive operators, ban repeat offenders, and seek restitution for consumers.

State attorneys general often have more direct impact for individual owners. They enforce state UDAP statutes and timeshare-specific laws. They can seek restitution, civil penalties, and injunctions. In some cases, filing a complaint may also lead to faster local action.

State real estate and timeshare regulators deal with licensing issues. If a resale company took fees without proper licensing or failed to use required escrow accounts, a complaint to the right state agency can lead to disciplinary action.

Refunds, Rescission, Civil Claims, and Other Consumer Remedies

If money has already changed hands, act fast on refund and rescission options.

If you paid by credit card, file a chargeback right away. Dispute deadlines are short and vary. A chargeback is not guaranteed, but it can be one of the fastest ways to try to get your money back if your records show the service was not delivered as promised.

Beyond chargebacks, owners may seek rescission, refunds, or civil claims under state consumer-fraud, fraud, or contract law. Some states allow attorney’s fees if you win. Statutes of limitation vary – often 2–4 years for consumer fraud claims, and sometimes longer for written contracts – so don’t sit on your paperwork. Waiting too long can shut down refund and claim deadlines.

Records Owners Should Keep if They Suspect Fraud

Good records make complaints and refund claims much easier to prove.

Stop paying at the first warning sign. Then document everything.

The records that help most are:

- The signed service agreement

- Payment receipts or card statements

- All emails and text messages with the company

- Any advertising materials or website screenshots that made specific promises

- A written log of phone calls with dates, times, and what was said

Save emails as PDFs, screenshot websites before they disappear, and back up text messages. That extra step can make a big difference later.

| Issue | Strong documentation | Weak documentation |

|---|---|---|

| Refund request | Written contract, receipts, and messages support the demand | Mostly verbal claims with little proof |

| Agency complaint | Clear timeline and copies of ads help investigators | Missing dates and missing documents slow review |

| Legal claim | Specific evidence strengthens facts and damages | Limited records make proof harder |

| Disputed promises | Emails or texts can show what was represented | No written record of promises |

File complaints with the FTC, your state attorney general, the attorney general where the timeshare is located, and the relevant real estate or timeshare regulator. Be specific. Include business names, websites, dollar amounts, and dates.

Investigators move faster when the facts are laid out clearly.

Legal Help for Owners Facing Timeshare Resale Problems

If complaints, chargebacks, and cancellation rights haven’t fixed the issue, the next move is a legal review.

At that point, don’t keep going back and forth with the resale company. If the reseller already took your money or left you on the hook, have a lawyer look at the case. That includes cases where you paid upfront fees and got nothing, signed a transfer agreement, or still remain liable under the original timeshare contract. A lawyer can review the paperwork and tell you whether the resale actually ended your original obligations.

When to Hire a Timeshare Attorney

Some situations call for legal help instead of more calls and emails with a resale company.

Talk to a timeshare attorney if:

- you paid upfront fees and received nothing in return

- you signed a transfer agreement but were never formally released from your original contract

"Even if you could ‘sell’ the timeshare to a third party, this still would not get you out of the original contract with your timeshare company without a formal release." – Aaronson Law Firm

That point matters. A resale does not cancel the original contract unless the developer gives you a formal release.

There are other warning signs too. Be careful if someone asks for a power of attorney or says the FBI or Treasury is involved. The same goes for claims about subpoenas or arrest threats tied to payment demands. According to the FBI and FTC, those are common signs of timeshare resale fraud, not normal business practice.

If any of this sounds familiar, stop sending money and cut off contact right away.

Before your first call with an attorney, pull together the key records:

- your original timeshare contract

- any resale service agreements

- proof of payment

- written correspondence

- marketing and solicitation materials

- credit reports, if missed payments or defaults are part of the issue

A clean paper trail makes it much easier for the attorney to review the facts right away.

How Aaronson Law Firm Helps Timeshare Owners

Aaronson Law Firm works only on timeshare-related legal matters. That focus can matter when the paperwork is messy or the resale company made promises that don’t line up with the contract.

Its services may include legal demand letters, formal rescission letters, and litigation support if the dispute gets worse.

If you still owe maintenance fees, assessments, or loan payments, resale may not be the best path. In some cases, a lawyer may decide that rescission is a better option.

Conclusion: Key Consumer Protections Owners Should Know

Timeshare resale fraud often leans on pressure, vague promises, and upfront fees. If that’s what happened, a timeshare lawyer can review rescission, credit protection, and litigation options. And if the contract is still binding or someone is still demanding money, legal help should be the next step.

FAQs

Can I still owe fees after a resale?

Yes. You’re still on the hook for all financial obligations tied to your timeshare until the ownership transfer is legally finalized.

That includes:

- Maintenance fees

- Special assessments

- Mortgage or loan payments

If you stop paying during the resale process, it can hurt your credit.

What if I already paid an upfront fee?

If you already paid an upfront fee to a reseller, there’s a good chance you were targeted by a timeshare resale scam. In most cases, legitimate companies collect payment only after the sale or transfer is complete.

Getting that money back can be hard, especially if the payment was made through methods that are tough to trace. You may want to contact Aaronson Law Firm to talk through your situation and possible legal options that may help protect your interests and credit.

How do I know if a reseller is legitimate?

Check the reseller’s credentials on your state real estate commission website to make sure they have a valid broker’s license. A legitimate company should be open about who they are, give you a clear written contract, and usually won’t ask for upfront fees.

Watch out for red flags like high-pressure sales tactics, unsolicited calls or emails, or promises of a guaranteed fast sale. It also helps to look up the company for scams or complaints and ask your timeshare developer whether the reseller is recognized.

Related Blog Posts

- How Courts Handle Deceptive Timeshare Sales

- How Consumer Protection Laws Impact Timeshare Complaints

- Avoiding Scams in Third-Party Timeshare Resales

- Timeshare Resale Scams: Case Studies