If you default on a timeshare, the damage can last for years. In many cases, it can hurt your credit for up to 7 years, add fees and interest to what you owe, lead to foreclosure or contract cancellation, trigger a lawsuit, and even create a tax bill if debt is forgiven.

Here’s the short version:

- Default usually starts after a 60- to 90-day cure period, not after just one missed payment

- Credit damage often shows up first, with late payments, charge-offs, collections, and sometimes a 150–200 point FICO drop

- Debt can grow fast from late fees, default interest, collection costs, and attorney’s fees

- Deeded timeshares may be foreclosed on, while right-to-use contracts may be canceled

- You may still owe money after foreclosure

- Lawsuits can lead to judgments, bank levies, liens, or wage garnishment

- Forgiven debt of $600 or more may lead to Form 1099-C and possible taxable income

If I were reading this to make a decision, I’d focus on one point first: ignoring the default usually makes the problem more expensive and harder to fix.

Quick Comparison

| Effect | How long it can last | Main risk |

|---|---|---|

| Credit damage | Up to 7 years | Lower scores, higher loan costs |

| Collections and charge-offs | Up to 7 years on credit reports | Bigger balance from fees and interest |

| Foreclosure or cancellation | Months to years, plus 7 years of credit harm | Loss of ownership or use rights |

| Lawsuits and judgments | Often 10–20 years, depending on state law | Garnishment, levies, liens |

| Forgiven debt taxes | Tax year of cancellation | IRS bill from canceled debt |

So the article’s core point is simple: a timeshare default is not just about missed payments. It can turn into a long credit, legal, and tax problem if you don’t deal with it early.

What Counts as a Timeshare Default in the U.S.?

A missed payment does not always mean you’re in default. In most cases, default starts only after the contract’s cure period ends. That window is often 60 to 90 days. After that, the developer or HOA may mark the account as in default.

In the U.S., default usually comes down to one of three duties.

Missed loan payments on a deeded timeshare can lead to foreclosure or repossession. If you took out financing to buy the timeshare interest and then stop making installment payments, you’re defaulting on a secured debt. The timeshare itself backs that debt.

Unpaid fees can become a lien, trigger collections, and lead to foreclosure. Annual maintenance fees and special assessments don’t just disappear if you stop paying them. They’re part of the contract, and the governing documents often let the association place a lien on the timeshare interest for unpaid amounts.

Points-based and RTU contracts can be terminated, with unpaid balances sent to collections and reported to credit bureaus. In plain English, the developer may cancel the membership and still go after what you owe through collections.

What happens after that depends on the contract, the kind of debt, and state law. Some states let a developer use nonjudicial foreclosure, which means no court case is needed. Others require a lawsuit, plus a judgment the developer has to win and enforce. In some cases, anti-deficiency rules may limit how much more they can try to collect.

Once default begins, the first long-term problem is usually credit damage.

sbb-itb-d69ac80

1. Credit Score Damage That Can Last Up to Seven Years

Credit score damage is often the first long-term fallout from a timeshare default. And it can start fast.

Once a timeshare account becomes delinquent, many developers report that missed payment activity to at least one of the three major U.S. credit bureaus: Experian, Equifax, and TransUnion. They don’t need to sue you to hurt your credit. The credit reporting alone can do plenty of damage. After the first late mark shows up, things can snowball as the account slips further behind.

That usually means a pattern like this:

- 30-day late payments

- 60-day delinquencies

- 90-day delinquencies

- charge-offs

- collections

If the default moves into foreclosure, the damage can be much worse. A timeshare foreclosure can sometimes cause a 150–200-point FICO drop, which is in the same range as a residential mortgage foreclosure.

Under the Fair Credit Reporting Act (FCRA), most negative marks stay on your credit report for about seven years from the date of first delinquency. If the debt gets sold or transferred, that seven-year period does not start over.

A lower score can push future borrowing into much higher-rate territory. And that matters. Even a modest rate bump can add thousands of dollars in interest over time. Credit card issuers may also cut your limits or shut accounts down altogether.

The hit is usually strongest during the first one to three years. After that, it tends to ease little by little as you build positive payment history on your other accounts. By years four through seven, scoring models often put less weight on older negative marks – but only if you don’t add new damage on top of the old. And while your score is taking that hit, the balance itself may keep growing through fees, charge-offs, and collections.

2. Collections, Charge-Offs, and Growing Debt Balances

After the credit hit, the debt usually doesn’t sit still. It grows. Once payments stop, fees and interest start stacking up, and the balance can get out of hand faster than most people expect.

The process usually follows a pretty familiar path. At first, the resort or developer handles collection efforts in-house. That often means reminder letters, phone calls, and late fees added to what you already owe. If the missed payments continue, the debt may be assigned or sold to a third-party collection agency. That’s when things often get more intense.

And it’s not just the original bill anymore. Timeshare contracts often allow for default interest, flat late fees for each billing cycle, collection agency fees, and attorney’s fees. All of that gets piled onto the unpaid amount. So a few hundred dollars in missed fees can turn into thousands over time as charges keep adding up month after month.

The longer the balance stays unpaid, the tougher it usually becomes to sort out. And that growing debt often sets the stage for the legal risks covered next.

3. Foreclosure or Repossession of the Timeshare Interest

If you stay in default, the resort, developer, or HOA may foreclose on the timeshare or end the contract. What happens next depends on one thing: whether the timeshare is deeded or contractual.

With deeded timeshares, the law usually treats the interest like real estate. So the process tends to look a lot like a standard home foreclosure. In many states, that means a nonjudicial power-of-sale process.

Right-to-use contracts work differently. Since they’re based on a contract, not real property, the resort will often send a default notice and cancel your membership rights if you don’t fix the default. In many cases, it doesn’t need to go through a real estate foreclosure at all.

The timing can vary a lot by state and by process. In some nonjudicial states, foreclosure can move from default to auction in about 4–6 months. Florida has also used a streamlined timeshare foreclosure process that can be finished in about 90 days after filing. In judicial states, where the resort has to file a lawsuit and get a court judgment, the process often takes 12–24 months.

But here’s the hard part: your credit can take a hit long before the foreclosure is over. Missed payments are often reported within 30–90 days. And once foreclosure proceedings start, that event itself may show up as a derogatory mark on your credit report.

Aaronson Law Firm‘s analysis found that 71% of timeshare mortgage defaults are reported to credit agencies, compared with 18% of maintenance-fee-only defaults. That gap matters. A foreclosure notation can stay on your credit report for up to seven years from the date of first delinquency. That can make it harder to get a mortgage, an auto loan, or better interest rates long after the timeshare is out of your hands.

And foreclosure doesn’t always wipe the slate clean. Even after the property is taken back, you may still owe money. The foreclosure filing also becomes part of the county public records, which means future lenders, landlords, and background-check services may be able to find it. If the sale doesn’t cover the full balance, the resort may go after a deficiency judgment.

4. Lawsuits, Court Judgments, and Wage Garnishment Risk

Foreclosure can end your ownership of the timeshare, but it doesn’t always wipe out what you still owe. The resort or HOA may still come after the deficiency – the unpaid balance left after foreclosure. And that balance doesn’t just sit there. It can keep growing, then turn into a separate collection lawsuit.

At that point, the matter can move into state court as a civil complaint. If you don’t answer the summons, the court can issue a default judgment. That means the creditor wins because you didn’t respond or show up. Put simply: no response can hand the case to the other side.

Once a judgment is entered, the creditor has more ways to collect. They may try:

- Wage garnishment

- Bank levies

- Property liens

Under the federal Consumer Credit Protection Act (CCPA), wage garnishment for consumer debts is limited to the lesser of:

- 25% of disposable earnings

- The amount by which weekly disposable earnings exceed $217.50

Some states give more protection. Texas, Pennsylvania, North Carolina, and South Carolina block wage garnishment for most consumer judgments. Even so, creditors in those states may still go after bank accounts or place liens on property.

There’s another hard truth here: judgments can stick around for a long time. Depending on state law, they may last 10 to 20 years and can sometimes be renewed.

Don’t ignore a lawsuit summons. Getting legal help before the deadline passes gives you more room to act. Aaronson Law Firm can review the contract, send demand letters, and help challenge collection steps.

5. Tax Consequences From Canceled or Forgiven Debt

Foreclosure or settlement may end the timeshare problem, but it can also set up a tax problem.

In many cases, the IRS treats forgiven timeshare debt as cancellation of debt income, often called COD income. Why? Because once the lender wipes out part of what you owe, that unpaid amount can be treated like income for tax purposes. The tax bill depends on how much debt gets forgiven.

Here’s a simple example. If you owe $20,000 and the lender agrees to cancel $10,000 in a settlement, that $10,000 may be taxable income for that year. At a 22% federal tax rate, that could mean about $2,200 in federal tax alone, before any state tax is added. So a person expecting a refund could end up owing money instead.

Lenders are generally required to file Form 1099-C with the IRS and send you a copy when $600 or more in debt is forgiven. That form shows the canceled amount and the date of cancellation. And here’s the part that trips people up: even if the form never makes it to your mailbox, you may still need to report that income. If a 1099-C gets filed and you leave it off your return, you could end up with an IRS notice or even an audit.

There are some exceptions to this rule. For example:

- If your debts were more than your assets when the debt was canceled, you may be able to exclude some or all of that income.

- Debt discharged in bankruptcy is also generally excluded.

To claim an exclusion, use Form 982 and keep records that show insolvency or bankruptcy. This is where things can get a little tricky, because the tax rules are technical and not always easy to read at first glance. For that reason, it can make sense to speak with a CPA or tax attorney before you lock in any settlement.

The timing makes this easy to miss. The ownership mess may feel finished, and then the tax issue shows up later like an unwelcome surprise in the mail. Next, compare how fast each timeshare default effect tends to show up and how long it can stick around.

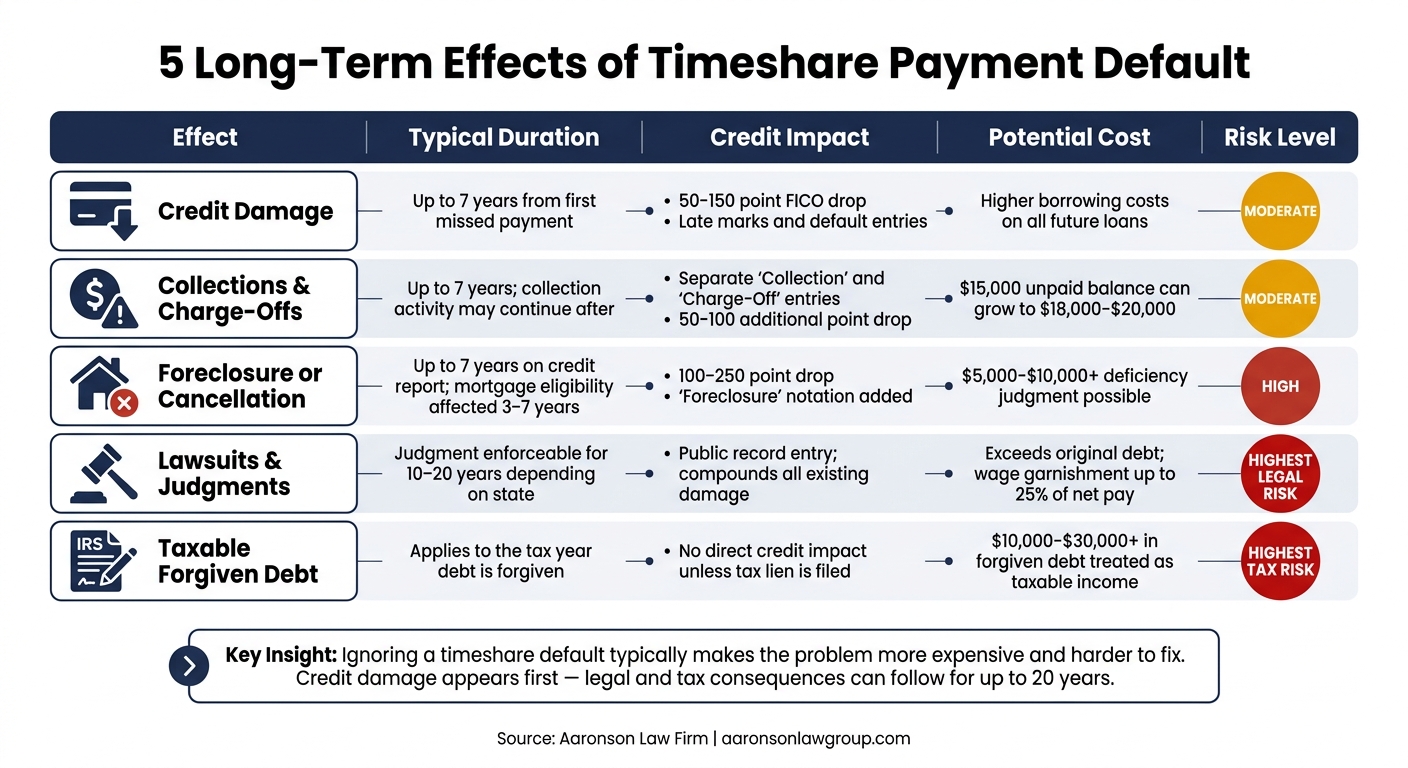

How Each Effect Can Impact You Over Time: A Quick Comparison

5 Long-Term Effects of Timeshare Default: Duration, Cost & Risk

The chart below boils the five outcomes down into one side-by-side view. If you want the fastest way to compare the long-term effect of each one, this is it.

| Effect | Typical Duration | Credit Impact | Potential Cost | Legal or Tax Risk |

|---|---|---|---|---|

| Credit damage | Up to 7 years from the first missed payment | 50–150 point FICO drop; late marks and default entries | Higher borrowing costs across future loans and credit lines | Low direct legal risk; high financial impact on future borrowing |

| Collections and charge-offs | Up to 7 years; collection activity may continue after the report date | Separate "Collection" and "Charge-Off" entries; 50–100 additional point impact | A $15,000 unpaid balance can grow to $18,000–$20,000 after fees and interest | Moderate; debt may be sold to collectors, and lawsuits are still possible |

| Foreclosure or cancellation | Up to 7 years on the credit report; mortgage eligibility affected for 3–7 years | 100–250 point drop; "Foreclosure" notation | Possible $5,000–$10,000+ deficiency judgment; tens of thousands in extra mortgage interest over time | Moderate; deficiency claims possible depending on state law |

| Lawsuits and judgments | Judgment enforceable for 10–20 years depending on state | Public record entry; compounds existing damage | Total cost can exceed the original debt due to legal fees, interest, and ongoing garnishment | Highest legal risk; court-ordered wage garnishment up to 25% of net pay, bank levies, and property liens possible |

| Taxable forgiven debt | Applies to the tax year the debt is forgiven | No direct credit impact unless a tax lien is filed | $10,000–$30,000+ in forgiven debt may be treated as taxable income | Highest tax risk; IRS Form 1099-C may be issued |

The big split here is timing. Some damage shows up fast, especially on your credit report. Other problems take longer to hit, but they can stick around for years through court action or tax bills.

When Legal Help May Be Worth Considering

Once a default reaches collections, foreclosure, or court action, legal help can help limit the fallout. This is usually the point where deadlines start to matter a lot, and even a short delay can make things worse.

If the contract itself may be disputed, an attorney can step in and review the paperwork and billing history. That may apply if there was misrepresentation, surprise fee increases, or charges that don’t line up with what was promised during the sales presentation. A lawyer can look for enforceability issues, spot billing problems, and help decide what to do before key response deadlines pass.

There’s also a practical upside once you have counsel. Under the Fair Debt Collection Practices Act (FDCPA), third-party debt collectors generally must communicate through your attorney. That can take some of the heat off and give you room to respond more carefully instead of reacting under pressure.

Aaronson Law Firm focuses on timeshare cancellation and offers free consultations, demand letters, credit protection, and litigation support.

Conclusion

A timeshare default can hit from a few angles at once: credit damage, collections, foreclosure, lawsuits, and possible tax liability. And once the account slips past due, those problems can stick around for a long time.

If the default process has already begun, start with the records that matter most. Pull your credit reports from AnnualCreditReport.com. Then review your original contract and check for any clause that limits personal liability or deficiency claims. Also watch for IRS Form 1099-C if any part of the debt was canceled or forgiven. That forgiven amount may count as taxable income, so it’s smart to speak with a CPA before you file your tax return.

Ignoring a default often means more debt, more legal risk, and more tax trouble. If you’re dealing with collection activity or a lawsuit, or you’re thinking about canceling the contract, Aaronson Law Firm offers free consultations for timeshare-related legal issues and can help you figure out whether cancellation or another legal remedy may fit your situation.

FAQs

Can I stop a timeshare default before foreclosure starts?

Yes. If you act before foreclosure starts, you may still have room to stop it.

Your first move should be to contact your timeshare company right away and ask about options like:

- Temporary payment reductions

- Extended repayment terms

- Short-term deferrals

That said, keep making payments until you have a formal agreement in place. That can help protect your credit and keep the situation from getting worse.

If those options don’t work, Aaronson Law Firm can help with timeshare contract cancellation, demand letters, and credit protection.

Will I still owe money after losing the timeshare?

Not always. Even after foreclosure, you may still owe a deficiency balance if the timeshare sale doesn’t cover the full amount you owed, plus interest and legal fees.

In many states, creditors can go after that unpaid balance through court judgments. That can lead to wage garnishment, bank levies, or liens on your property. And if some of the debt gets forgiven, the IRS may count that forgiven amount as taxable income.

Do maintenance fee defaults hurt credit too?

Yes. Missing maintenance fee payments can hurt your credit score if the delinquency is reported to the credit bureaus.

That said, this kind of reporting is less common than what you usually see with loan defaults. But it does happen.

If it’s reported, the negative mark can stay on your credit report for up to seven years.

Aaronson Law Firm offers timeshare-related legal services, including credit protection and dispute assistance.

Related Blog Posts

- How Timeshare Payment Plans Affect Credit Scores

- Timeshare Debt After Cancellation: What To Know

- What Happens After Timeshare Foreclosure?

- Timeshare Cancellation and Credit: Common Problems, Solutions