Timeshare financial disputes are becoming more common, with rising maintenance fees, high-interest loans, and rigid contracts creating challenges for owners. Recent legal cases highlight growing scrutiny over deceptive sales practices, financial obligations, and consumer protections, particularly for military personnel. Key takeaways include:

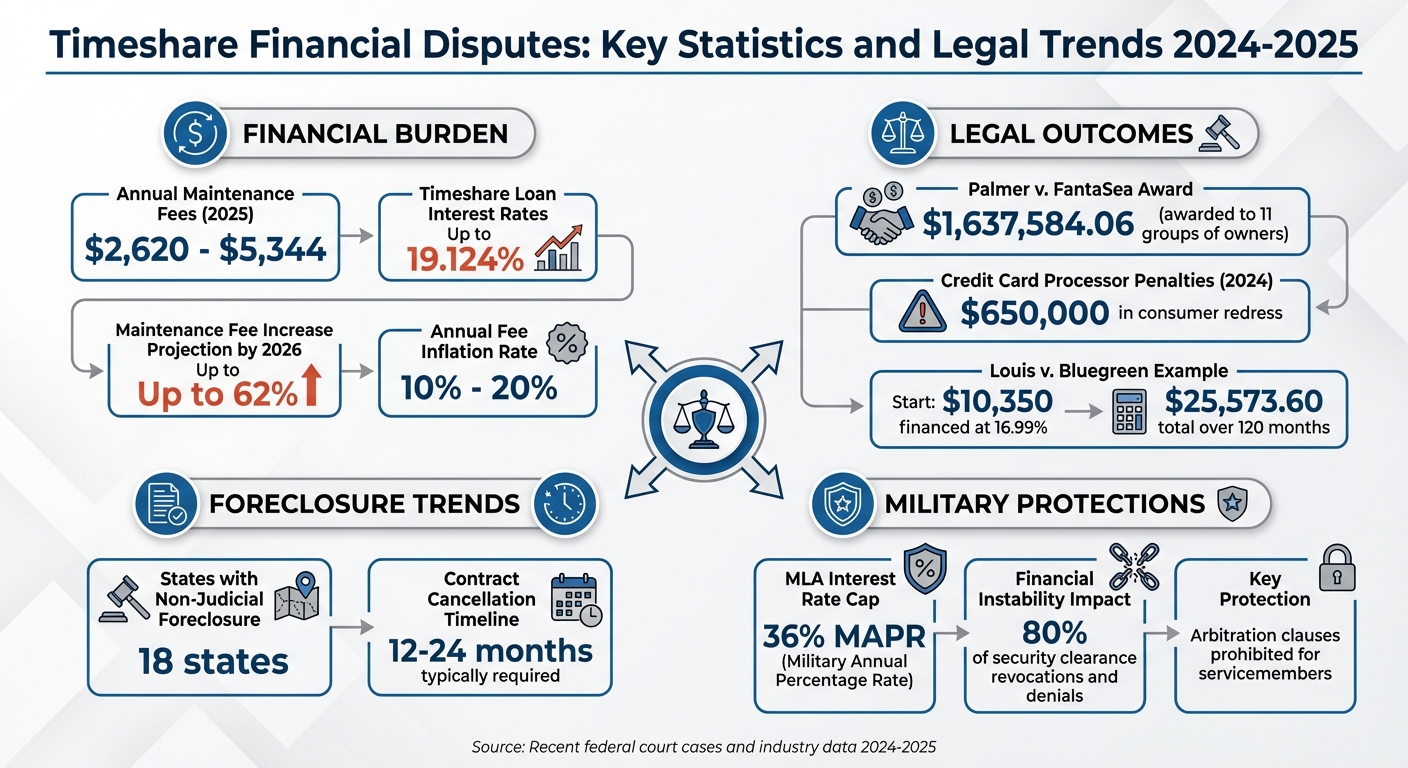

- Maintenance Fees: In 2025, fees ranged from $2,620 to $5,344 annually, with special assessments adding strain. Defaults are rising, leading to foreclosures.

- High-Interest Loans: Timeshare loans often carry interest rates up to 19.124%, doubling the original cost over time.

- Legal Trends: Courts are addressing deceptive sales tactics and arbitration clauses, as seen in Palmer v. FantaSea, which awarded over $1.6 million to owners for misleading guarantees.

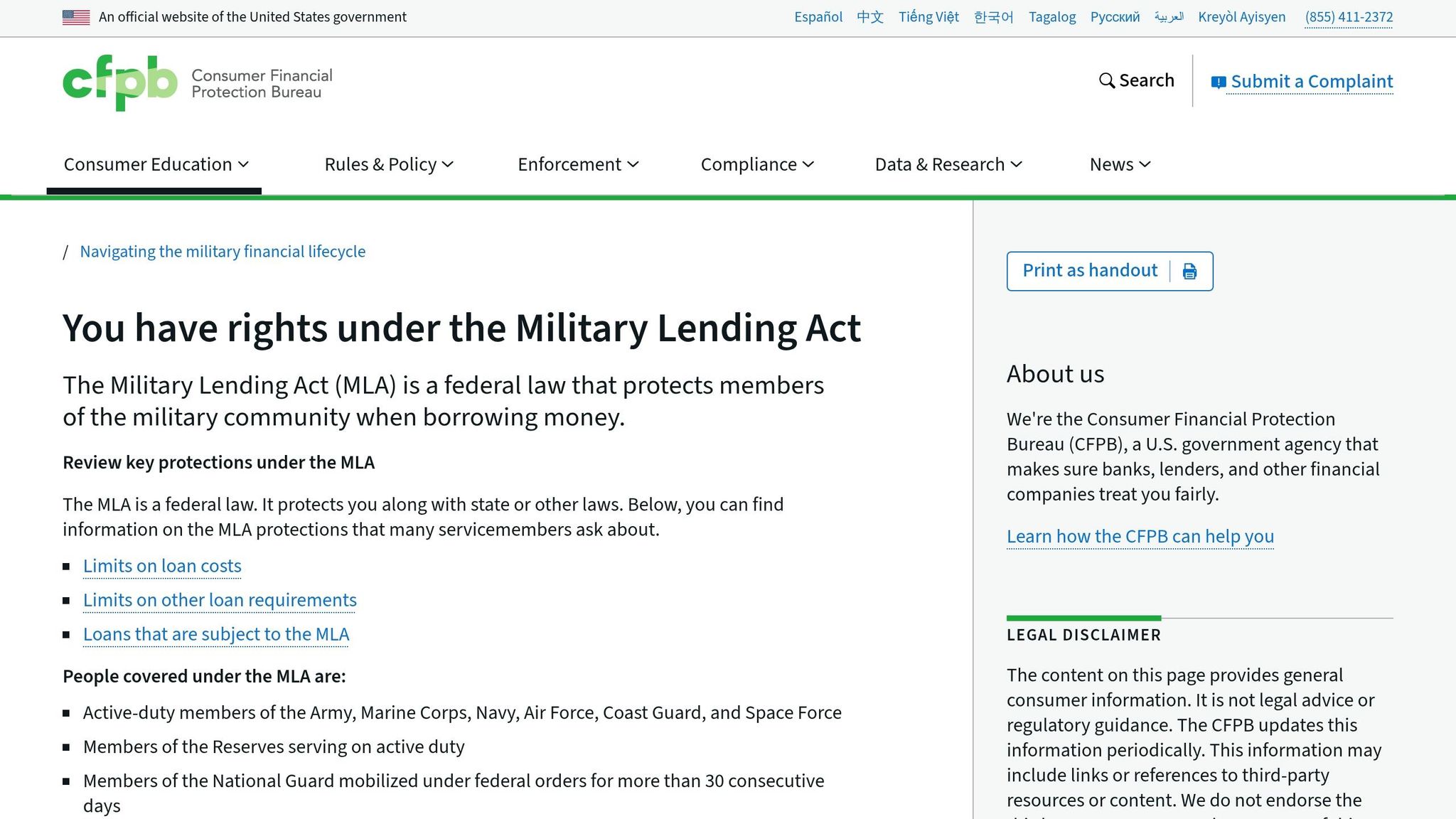

- Military Protections: The Military Lending Act (MLA) caps interest rates and prohibits arbitration clauses for servicemembers, impacting timeshare agreements.

- Foreclosures: Developers increasingly use non-judicial foreclosures, which can leave owners with tax liabilities and unresolved credit issues.

Understanding these trends is crucial for navigating timeshare disputes. Legal expertise is often necessary to challenge contracts, protect finances, and explore exit options effectively.

Timeshare Financial Disputes: Key Statistics and Legal Trends 2024-2025

Recent Changes in Timeshare Case Law

Over the last two years, courts have begun taking a closer look at timeshare disputes, moving beyond simple contract issues to examine questionable sales practices and potential consumer protection violations.

How Courts Now Interpret Financial Obligations

Federal courts are now paying more attention to how developers structure financial obligations in timeshare agreements. Two rulings from the U.S. Court of Appeals for the Eleventh Circuit in 2024 highlight this evolving perspective.

In Steines v. Westgate Palace, LLC (September 2024), the court ruled that the Military Lending Act (MLA) takes precedence over the Federal Arbitration Act (FAA) for timeshare loans involving active-duty servicemembers. Adam Steines, an Army servicemember, questioned the legality of an $8,024.87 loan from Westgate, citing the company’s failure to provide mandatory interest rate disclosures. The court concluded that timeshares qualify as "transient lodgings" rather than "dwellings", which means they don’t fall under the residential mortgage exception. As a result, arbitration clauses in such agreements cannot be enforced against military members.

Circuit Judge Marcus explained:

The question of whether the FAA has been overridden by another congressional enactment necessarily precedes the court’s enforcement of any arbitration agreement, including a delegation clause, and always belongs to the court.

However, not all outcomes lean toward consumer protection. In Holden v. Holiday Inn Club Vacations Incorporated (April 2024), the court addressed disputes over credit reporting. Tanethia Holden and Mark Mayer stopped paying on their timeshare contracts, claiming they had canceled them, but Holiday Inn continued reporting the debts as delinquent to Experian. The court ruled that the complex contract interpretations involved made the dispute unsuitable for claims under the Fair Credit Reporting Act. Circuit Judge Luck clarified:

Whether the alleged inaccuracy is factual or legal is beside the point. Instead, what matters is whether the alleged inaccuracy was objectively and readily verifiable.

These cases indicate a shift in how courts approach timeshare disputes, opening the door for new litigation approaches, including consolidated lawsuits.

Class Action Lawsuits and Their Outcomes

Traditional class actions are being replaced by consolidated multi-plaintiff litigation, which allows courts to address systemic issues while still considering individual circumstances.

In Palmer v. FantaSea (April 2025), eleven groups of timeshare owners brought a consolidated case against a developer accused of making verbal guarantees during sales presentations that directly contradicted the written contracts. The appellate court awarded $1,637,584.06, which included trebled damages and a 25% fee enhancement due to the high risk involved in prosecuting the case. The court rejected the developer’s use of the parol evidence rule as a defense, stating:

[The timeshare developer] advocates for a legal bait-and-switch in which it offers certain guarantees during its sales pitch, only to explicitly contradict those guarantees in its contracts… we would, in effect, give license to the use of the parol evidence rule as a sword to aid and abet deceitful sales practices. We decline to do so.

In addition to addressing deceptive sales tactics, courts are also targeting the financial systems that enable fraud. In 2024, credit card processors that supported timeshare exit schemes were ordered to pay $650,000 in consumer redress following investigations by the Department of Justice and Federal Trade Commission. Regulators found that these processors ignored warning signs, such as unusually high chargeback rates, making them complicit in the fraudulent activities.

These rulings reflect a growing effort to hold both timeshare developers and their financial partners accountable, signaling a broader push to dismantle the systems that allow fraudulent practices to thrive.

Military Lending Act (MLA) and Consumer Protection Cases

The Military Lending Act (MLA) plays a crucial role in timeshare litigation, especially as developers face growing scrutiny over loan arrangements for active-duty servicemembers. Under the MLA, interest rates are capped at 36% (Military Annual Percentage Rate or MAPR), specific oral and written disclosures are required, and mandatory arbitration clauses are prohibited in contracts involving military personnel. Violations of the act render loans void from the start, as stated in 10 U.S.C. § 987(f). These provisions continue to shape legal battles over timeshare financial agreements.

Louis et al v. Bluegreen Vacations Unlimited, Inc.

In September 2021, Private Emmanuel Louis and his wife filed a class-action lawsuit against Bluegreen Vacations in the Southern District of Florida. They had financed $10,350 at a 16.99% interest rate, which totaled $25,573.60 over 120 months. The lawsuit alleged that Bluegreen violated the MLA by including a mandatory arbitration clause in the contract and failing to provide the required MAPR disclosures.

Although the case initially garnered support from federal agencies, the outcome took an unexpected turn. In June 2024, the 11th Circuit Court of Appeals upheld the dismissal of the case. The court ruled that the Louises lacked standing because their financial injury – specifically, a $1,600 down payment and monthly payments – was not directly linked to the disclosure failures. The court stated:

The fact that the contract may be void serves merely as a possible remedy… It does not establish causation between the alleged payments and the alleged violations.

This decision raised concerns among consumer advocates. The Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) filed a joint amicus brief, warning that the ruling "would substantially curtail enforcement of the MLA" and would "bar service members from bringing suit unless they can show that the alleged violation of the MLA was material to their decision to take out the loan." In January 2025, the U.S. Supreme Court declined to review the case, leaving servicemembers in the 11th Circuit with limited options for legal recourse.

Supreme Court and Advocacy Group Involvement

The Louis case attracted significant attention from military and consumer advocacy groups. Organizations such as the Military Officers Association of America (MOAA), Blue Star Families, Iraq and Afghanistan Veterans of America, and the National Military Family Association filed amicus briefs urging the Supreme Court to hear the case. These groups highlighted the dangers of predatory lending practices, emphasizing how they undermine servicemembers’ financial stability and, by extension, national security. Financial instability is a major concern, accounting for 80% of security clearance revocations and denials. Rose Carmen Goldberg, Associate Director of Policy and Programs at Stanford Law School, noted in her brief:

Financial readiness is a crucial aspect of military operational readiness… the Eleventh Circuit’s evisceration of the Act’s protections weakens national security.

Although the Supreme Court’s refusal to hear the case was a setback, regulatory efforts to protect servicemembers persist. For example, in July 2025, the CFPB reached a settlement with FirstCash, Inc. over MLA violations, signaling continued enforcement against lenders who fail to comply with the law. These regulatory actions reflect ongoing efforts to safeguard the financial well-being of military personnel.

Developer Financial Practices and Court Responses

Recourse Notes and Owner Liabilities

Timeshare developers typically use promissory notes to finance purchases, spreading payments over the long term. These notes are backed by the vacation ownership interest (VOI) itself, but the financial implications for owners often go far beyond the initial cost. Courts are now wrestling with how these financing agreements align with unclear default clauses.

At the heart of the issue is what happens when owners default. Many owners assume that default means the developer keeps their prior payments as liquidated damages and the contract ends. Developers, however, often interpret the same terms differently – they believe they can repossess the timeshare and continue reporting the full outstanding balance to credit bureaus. Florida state courts have issued conflicting rulings on nearly identical contract language. For instance, in Holiday Inn Club Vacations v. Granger, the court sided with the developer, awarding a deficiency judgment. But in Orange Lake Country Club, Inc. v. Arndt, the court ruled that the developer could not collect further payments after default.

This legal divide in Florida also affects credit reporting practices. Owners often face a costly and time-intensive process of obtaining a court ruling to confirm they no longer owe the debt before they can challenge how it’s reported to credit bureaus. This legal murkiness has led to inconsistent outcomes in repossession cases, which are further explored below.

Repossession Trends and Default Cases

The uncertainty surrounding default clauses has also shaped repossession practices across various states. The timeshare industry is increasingly turning to non-judicial foreclosure methods in 18 states, bypassing court involvement. These processes allow developers to repossess timeshares without filing lawsuits. Under Florida law (Fla. Stat. § 721.81), developers cannot pursue deficiency judgments after a non-judicial foreclosure – provided the owner does not object – meaning they cannot claim the difference between the debt owed and the timeshare’s value.

However, most owners do not contest these foreclosures. Attorney Kurt P. Gruber observes:

Defendants generally do not contest these foreclosure actions. In most cases, they do not appear in court or respond to the complaint, and often do not acknowledge the existence of the foreclosure proceedings.

This lack of participation often suggests that owners are primarily focused on exiting their financial obligations. When developers write off these unpaid balances, they report the amounts to the IRS using Form 1099-C, effectively converting the debt into taxable income for the owner.

sbb-itb-d69ac80

What These Trends Mean for Timeshare Owners

Understanding Your Rescission Rights

Recent legal developments have expanded the rights of timeshare owners, giving them more opportunities to rescind contracts under certain circumstances. Court cases like Palmer v. FantaSea have shown that rescission rights can go beyond the usual cooling-off period, particularly when developers use deceptive sales tactics. These rulings highlight the growing recognition of consumer protections in timeshare agreements.

For active-duty servicemembers, protections under the Military Lending Act (MLA) have been reinforced. Courts now allow servicemembers to bypass mandatory arbitration clauses and take their cases to federal court when timeshares are classified as "transient lodging" rather than residential mortgages.

In addition, owners in 18 states can still opt for judicial foreclosure review, even in states that primarily use non-judicial foreclosure processes. This means developers cannot pursue personal deficiency judgments after repossession in these states. However, choosing judicial review requires a careful look at your contract and circumstances, as it involves a different legal process. Understanding your options is key to navigating these situations effectively.

Why Specialized Legal Help Matters

Given the complexities of timeshare contracts, having access to specialized legal expertise is essential. These agreements often include intricate language that can make it difficult to identify valid reasons for termination. Courts have consistently emphasized the need for specialized knowledge in real estate law and federal consumer protection statutes to challenge deceptive practices successfully.

Aaronson Law Firm specializes in helping timeshare owners cancel their contracts. They offer services like free consultations, demand letters, credit protection, and litigation support. Their attorneys are skilled at uncovering discrepancies between sales presentations and written contracts, challenging illegal arbitration clauses, and guiding clients through the 12 to 24 months typically required to cancel a contract. With maintenance fees rising by 10% to 20% due to inflation, working with a dedicated legal team can help safeguard your finances and prevent mounting costs over time.

Conclusion

Timeshare case law is shifting, and staying informed is crucial to protecting your financial interests. Courts are taking a closer look at misleading sales tactics, as shown by recent decisions that penalized such practices. On the other hand, protections under the Military Lending Act have been strengthened, allowing active-duty servicemembers to bypass arbitration clauses and take their claims directly to federal court.

Still, not all developments work in favor of consumers. For instance, disputes about credit reporting remain murky. Courts have ruled that credit agencies aren’t obligated to resolve disagreements over contracts unless the inaccuracies can be objectively proven. This highlights how court interpretations in timeshare disputes can vary widely.

Adding to the challenge, maintenance fees are climbing at a rapid pace – some estimates suggest increases of up to 62% by 2026. Combined with inconsistent rulings on identical contract provisions, the stakes in these cases have never been higher. The outcome of a dispute often hinges on the legal precedents in your jurisdiction, making expert legal guidance essential.

Aaronson Law Firm specializes in timeshare contract cancellation, offering the expertise needed to tackle these complex issues. Their attorneys are skilled at challenging illegal arbitration clauses, exposing discrepancies between sales presentations and contracts, and helping clients navigate the legal process while safeguarding their credit and finances. Taking action now can help you avoid rising fees and achieve a clean break from your timeshare commitments.

FAQs

Can I challenge a timeshare contract based on what the salesperson promised?

Yes, it’s possible to dispute a timeshare contract if the salesperson made deceptive or misleading promises. In the U.S., recent legal trends have leaned toward protecting consumers, with courts often nullifying contracts tied to tactics like high-pressure sales, false claims, or incomplete disclosures. Time is of the essence, though – many states have specific rescission periods during which you can cancel the agreement. Seeking legal help can strengthen your case, especially if dishonest sales practices are part of the issue.

How does defaulting affect my credit and what I still owe?

Defaulting on your timeshare payments can create serious financial and credit issues. Missing payments often results in late fees, added interest, and a noticeable hit to your credit score. If the nonpayment continues, you could face foreclosure, long-lasting credit damage, and even deficiency judgments, where you’re held responsible for the remaining balance after foreclosure. Keep in mind, unless your contract is legally canceled, you’ll still owe what’s left on the loan. Consulting with a legal professional can help you navigate these challenges and potentially reduce the financial fallout.

Do active-duty servicemembers have special rights under the Military Lending Act?

The Military Lending Act (MLA) provides special protections for active-duty servicemembers, particularly when it comes to predatory practices in timeshare loans. These safeguards include a cap on interest rates, which cannot exceed 36%, and a prohibition on mandatory arbitration clauses. If a timeshare agreement violates these rules, it may even be rendered void. These measures are designed to protect servicemembers from unfair financial burdens often associated with timeshare contracts.

Related Blog Posts

- How Courts Handle Deceptive Timeshare Sales

- Timeshare Owners’ Associations and Fee Regulations

- Landmark Cases vs. Modern Timeshare Disputes

- How Consumer Protection Laws Impact Timeshare Complaints